We are absolutely living in a world encapsulating Power, Nature, Love and Relationships, and Conflicts.

As humans, we have hopefully learned, especially in a crisis, our emotions have a powerful and growing influence over our short-term investment decisions. Which by itself poses a conflict as investing is meant to be a long-term endeavor.

During times like today, where there is plenty of negative news about the economy, the markets and perhaps our personal lives as well, it can be difficult to think longer term. It is hard watching a portfolio decline in value as our natural aversion to losses can lead us to consider selling our investments and riding out the storm in cash.

However, despite the short-term relief one may feel, with the likely absence of fortuitous timing, the feel-good action of turning to cash could create a negative impact on your long-term plan. We understand each crisis and market reaction is different, however, the longer your anticipated time horizon and the more fine-tuned your financial plan, the more you should consider staying the course.

“Staying the course” should not be confused with doing nothing. During periods of unusual volatility, tax management, portfolio rebalancing and opportunistic purchasing can create tremendous long-term value. But if you are still considering hitting the sell button and parking your money under the proverbial mattress (though with some parts of the world offering negative rates of interest it’s a thought), here are some considerations you need to keep in mind.

LOSS OF PURCHASING POWER

Over long periods, holding large amounts of cash can destroy wealth as its purchasing power is eroded by rising costs. There can be no guarantee costs will continue to inflate-but we think they will longer term. On the welcome thought of spending Thanksgiving with loved ones this year, let’s look at the appreciation of the main course. In 1999 you would pay on average, $0.98 per pound for your Thanksgiving turkey. The same turkey, 20 years later, would cost $1.39 per pound. That is an increase of 40%+ over that time frame. Said it another way, $1 in the future will not get you the same things as it does today, all thanks to inflation, the silent killer of purchasing power.

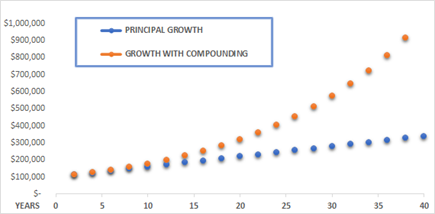

THE POWER OF COMPOUNDING

Having a prudent asset allocation will help reduce significant drawdowns, thus decreasing the need to go to cash and foregoing the power of compounding over time. Albert Einstein famously said that “Compound interest is the eighth wonder of the world. He who understands it, earns it…he who doesn’t … pays it.” Compounding means that you earn return not only on the invested principal but also on the growth/interest that you received. In other words, you are getting interest on interest, which allows your money to grow at a much faster rate. As the chart below depicts, in the early compounding periods, the interest portion is small. But if you earn steady returns on your investments over a long period of time, the power of compounding becomes a big deal and will have a huge impact on your assets.

OPPORTUNITY COSTS CAN BE HUGE…

Opportunity costs represent the benefit an individual or investor misses out when choosing one alternative over another. In this case, it would mean the return received from holding cash instead of an allocation to stocks and bonds. Over a three month or for that matter three year period, we cannot accurately predict how the returns of financial assets will compare to cash holdings. History strongly suggests in a capitalist world we will earn sufficient premiums for placing capital at risk.

To put this into context, think about the following. $100 deposited into a bank account in 1970 would only be worth $944 as of the end of 2019 assuming annual interest received was the same as 3-month Treasury bills. The same $100 invested in 10-year US Treasuries would be worth $2,940 and more astonishingly an investment in the S&P 500 would grow to $14,821 on a total return basis. Please note this time frame includes the 1973-74 bear market, the 1987 “crash”, the dot-com bust and Great Recession of 2008-2009.

MARKET TIMING IS TEMPTING…

…But unlikely to be successful. Years of research have shown that it is nearly impossible to effectively time the markets repeatedly, even for the most experienced managers. Successful market timing requires two things: (1) knowing when to sell out of the market, and (2) knowing when to get back in. The odds are against you to accurately time these decisions, and the cost of attempting to time the markets can be high and presents a real danger. As humans, we can be our own worst enemy when it comes to short-term oriented portfolio managementdecisions during times of crisis.

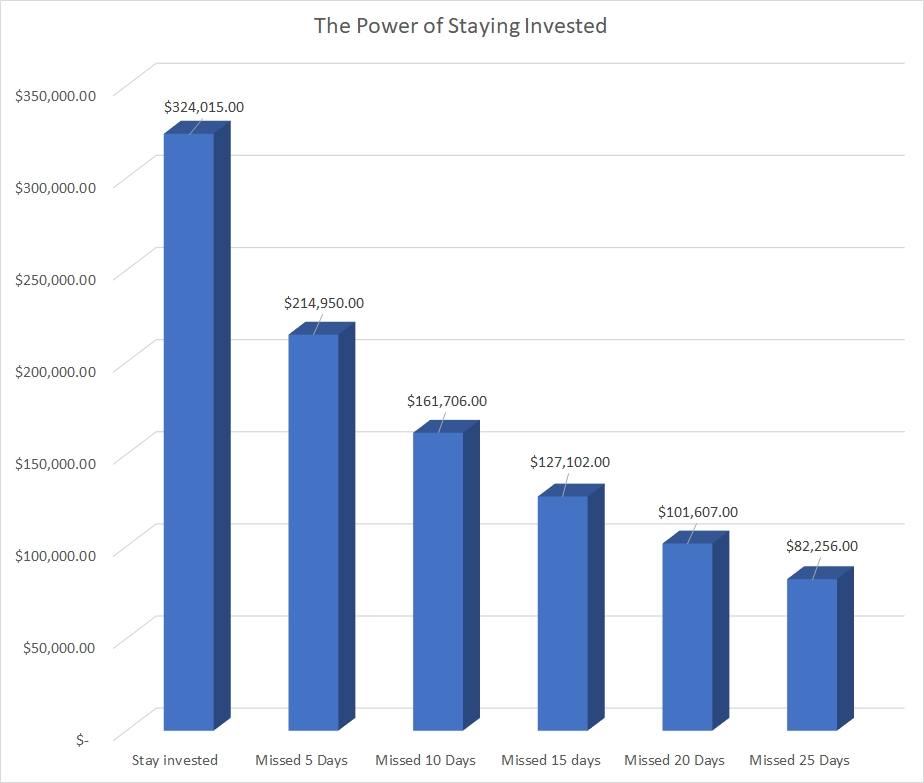

When market volatility spikes, many investors sell at market lows (by definition, when things feel the scariest) and buy after returns have improved – often missing the best days in the market and dampening their long-term returns. Missing only a few days of strong returns can drastically impact overall performance over time. Often, the best days for stocks follow the worst days. As you can see below, over the last 20 years, missing just 10 best trading days would have a meaningful impact on returns -reducing the growth by 50%. And missing 25 days, would lead to the loss of principal. The stock market has been resilient throughout its history and stocks have recovered from short-term crisis events (look at the market crash of 1987, dot-com bust, 2008 financial crisis) to move higher over longer time periods.

Since we don’t have a crystal ball that can tell us when market volatility will spike again, our experience and academic research tells us that a diversified portfolio of stocks, bonds and alternatives gives investors a good opportunity to maximize investment return over time.

CONSIDER THE LONG-TERM PERSPECTIVE AND THE RIGHT MIX

History of course is not a guarantee of what the future may hold. If you are not able to stomach the ride and stay the course due to the short-term swings, you may find you end up not fully benefiting from the long-term appreciation we have been accustomed to in the financial markets. Considering your goals and ability to tolerate risk is crucial for enhancing your odds of achieving long-term success with investing. The right asset allocation should be conducive to staying invested over the long term – creating a smoother ride and investing experience.

Until we get to the final act of COVID 19 we cannot say with 100% confidence that cash does not have a place in your portfolio. Any allocation to cash must be viewed in the context of the overall financial plan. Cash will always remain an appropriate vehicle for short-term planned expenditures. Liquidity needs (expected or non-anticipated), as well as changes in life situations (divorce, loss of a job), should also be a consideration in determining appropriate levels of cash to have on hand. What you want to avoid is making decisions that are based on fear of market corrections, panic and human emotion.

While market volatility can be unsettling, a well-thought-out plan will put you on the path to accomplish your financial goals while exposing you to the level of risk that you can tolerate. At Withum Wealth Management we have the experience to help you develop and execute such a plan.