Defining a Role for Yield Oriented Investments

From our perspective, the world is more different today than in any previous decade we can remember. For income investors the world has turned upside down and then some. How strange is this: some global fixed income participants are looking at a negative rate environment-yes negative. So, you give me $1,000 and I return $990 in a year’s time – interesting concept.

Asset allocation decisions are something that all investors engage in, and those decisions historically remain relatively static through different market cycles, changing when our goals change. However, one dilemma all of us face today is how to generate sufficient portfolio income in a sub 1% rate environment. With interest rates at historically low levels around the world, what role do bonds play in a portfolio?

A Tool to Mitigate Volatility

In our eyes, bonds serve one major purpose in a portfolio above all else – mitigating volatility. Very few investors are wired to withstand the dramatic swings that the stock market experiences. Sure, stock market returns are historically better than bonds, but in many cases our behaviors get in the way of realizing stocks’ full potential return. Volatility (extremely high today) is the price we pay for higher returns. Bonds can reduce portfolio volatility to make it feel more tolerable, allowing investors to stay with their investment plans while producing some incremental cash flow.

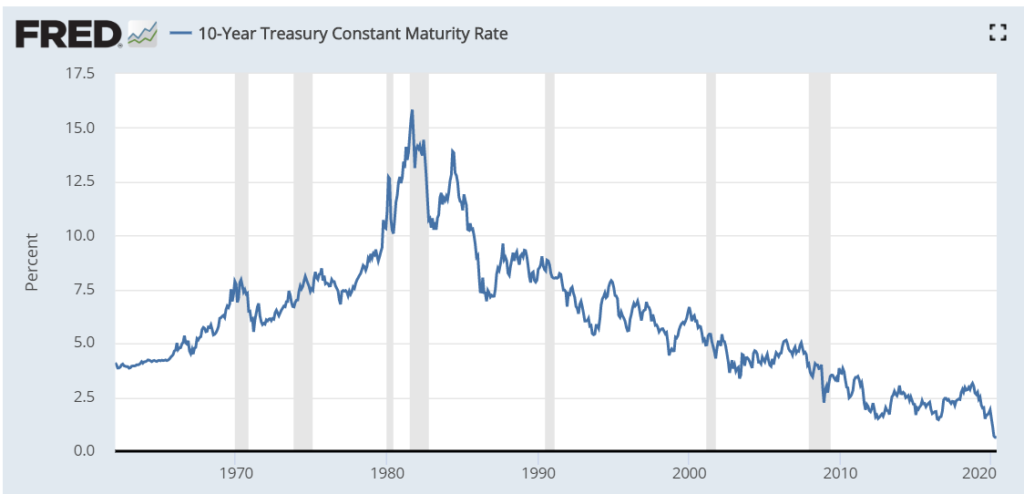

The current bull market in bonds is going on nearly 40 old. Since 1982, bond rates have been falling steadily from 15.8% to 0.6% for the 10-year US Treasury. In the early 1980’s mortgage rates and CD rates were yielding 12-15%. Inflation was also high and that was the catch.

Real Returns Matter

If a bond yields 8% and inflation is 5%, your real return is 3%. So, current inflation rates and projected future rates are important components in the fixed income decision process. Today, bonds appear to be offering real returns that are somewhat unattractive. Of course, one of the big unknowns associated with the COVID 19-related multi-trillion-dollar rescue packages is: will inflation begin to accelerate or despite these packages are we looking at lower or declining interest rates for an extended period? How you answer that question will impact what kinds of fixed income investments you should own.

Investing for Yield Can Be Full of Traps

Some income investments have a defined maturity such as a ten-year bond, but others do not. Perpetual investments introduce a new risk in terms of not having a guarantee you will get your initial investment returned in full. Therefore, we recommend not just searching for the highest yielding investment.

While yield is important, it should not be the only factor investors consider when choosing an investment. Several types of investments have above average yields; however, it is important to look at the potential downside too. What follows under this caption is a brief primer, not a recommendation, on income-related investments that in our unscientific polling seem to be gathering investor’s attention.

Master Limited Partnerships (MLPs) – MLPs are companies that trade publicly but are structured as limited partnerships. Combining the liquidity of a publicly traded company with the tax benefits of a private partnership, allows for income to be passed through from the company directly to shareholders. MLP’s are a common structure for pipeline operators. However, in times like today when oil demand is very low and oil supply is at or near capacity, pipeline companies take on a unique set of risks.

Many pipeline partnerships may or may not look attractive based on yield or a view on future fundamentals. However, it is important to understand that any investment can be subject to large swings in price. The key is to not let the current yield lead your decision-making process.

Real Estate Investment Trusts (REITs) – REITs are akin to MLPs but instead of pipelines they own or operate real estate related investments. REITs allow for indirect ownership of property instead of buying real estate outright. REITs can also achieve favorable tax treatment by paying a regulated percentage of income to shareholders. REITS come in many flavors including apartments, data storage, malls and commercial real estate to name a few.

In today’s economy, many businesses, property owners and renters are rethinking their working and living situations. Commercial real estate and mall ownership for example may be significantly less attractive as COVID-19 causes people to reexamine aspects of their lives.

Preferred Stocks – An alternative to common stock, the type of shares most investors hold, are preferred shares, which are higher up the chain in the capital structure of a company. Despite the reference to stocks in the name, there are a few key aspects of preferred stocks that make them more like bonds than equity.

First in the event a company cuts it common stock dividend, it may continue to pay the preferred share dividend. This may also mean that should a company enter bankruptcy, preferred shares could be paid out, or made whole, before common stockholders, but still after bond holders. Second, preferred shares can be called back by the company. Like bonds, preferred stocks are sensitive to changes in interest rates meaning the shares could be called back early at par or trade at a discount, regardless of the underlying company performance. Third, preferred stocks can have conversion features where the preferred shares convert to common stock in certain situations. An investor may want to keep holding the preferred, but gets converted to common stock, altering their asset allocation. These factors all play a role in deciding whether preferred stock is the right investment for each investor and her goals.

What is hopefully becoming apparent is that adding income to a portfolio today is as challenging as any time in recent memory. There is another way to add income to a portfolio but perhaps with a limited offset to portfolio variability.

What about stock dividends?

Dividends have been around for as long as companies have been publicly traded. The first recorded dividend was from the Dutch East India Company which was publicly traded from 1602-1800, paying out nearly 18% for almost 200 years of existence (though that included a return of capital as well).

Today, the S&P 500 has a dividend rate of about 2.1%, but when factoring in only the companies that pay dividends, the average rate is closer to 3%. Dividends have become more appealing for certain investors – and others may feel forced into dividend paying stocks, taking on additional equity risk in exchange for more meaningful income from bonds. Like all other investments price, yield and return on of principal matters.

In this pandemic, many notable companies which were once believed to be very stable have suspended or halted their dividends. Carnival Cruise, GM, Disney, Hilton Worldwide, Las Vegas Sands and Boeing are examples of recognizable companies that have suspended their shareholder dividends. The dividend suspension itself may or may not be an indicator of future stock performance, but it certainly impacts investors that were counting on the dividends.

At the end of the day we need to find balance in our investment choices. Yes, yield is important and can play an integral part in the investment process, but we must also focus on many other factors. Proper portfolio construction should look to meet your income needs but with an overarching view towards suitability and probability of success.

As always, if you have any specific questions about your portfolios, please do not hesitate to contact us and stay safe.