The economy seems to be at an inflection point.

On the one hand, restaurants are packed, planes are full, and traffic commuting to work is busier than ever. On the other, major tech firms are laying off tens of thousands seemingly every week and the media is hammering the word “recession” into our ears every time we turn on the television. So, what gives?

Just as you ponder the answer to this question, there are many questions that need to be answered when it comes to investing. Investing is not meant to be easy, but it can be with the right strategy and team. It is also important to differentiate the market from the economy to some degree.

Let us ask you this… would you be happy with an 8% return every year for the rest of your life? Probably, yes, right? This would simplify the answers to questions like…

- How much do I need to save for retirement?

- When can I retire?

- Will I be able to afford _____ goal by age ____? (fill in the blanks)

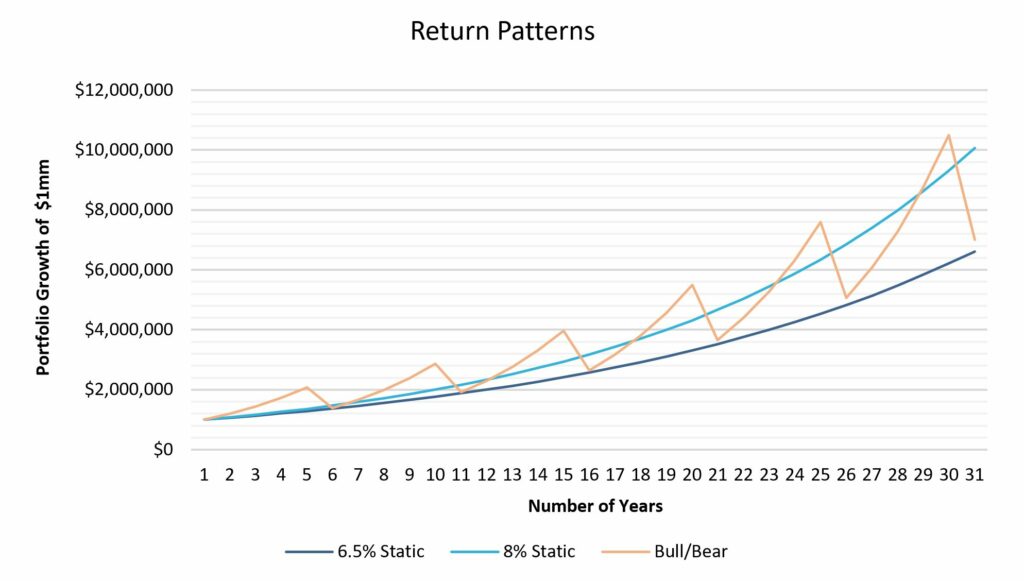

Despite all of those “compound interest” calculators online, there is no investment that gives us a constant 8% return year over year. What if we could get you a static 6.5% return? Would you be interested in that? It’s less than 8%, but you would not experience any volatility or most importantly, the stress and worries caused by volatility. Our gut tells us that most people will set unrealistic expectations – you may say you can stomach the volatility and go for the higher return, but when that volatility strikes, get nervous and change course by taking on or reducing risk assets at the wrong times. Be honest with yourself – have you held off on investing more money this year because last year was so bad? Have you ever accelerated an investment because everything was going up only to be let down soon after?

What if we shift our perspectives a bit… Let’s look at investing in five-year periods. The first four years, we’re going to get a 20% return per year, but that fifth year, we’re going to lose about a third of everything, down -33.3%. These return patterns are not too dissimilar to bull/bear market cycles. Some bull markets are longer and stronger – so are some bear markets. We bet it doesn’t feel like you are getting an 8% return every year.

Anyone who “guarantees” 6.5% per year is probably not telling the whole truth, but with interest rates higher today than last year, investors have more options to get a more stable return with portions of their portfolio. This allows for less exposure to more volatile investments while still meeting your goals. Hypothetically, if you focus on above average dividend paying stocks, yielding 2.5% with half of your portfolio and purchase some intermediate duration, corporate debt yielding 4.5% with the remainder, your portfolio is yielding 3.5%. This is a far too simple analysis, but more than half of your 6.5% return bogey is accounted for assuming no growth for the stocks! It is so important to put your emotions aside and continue saving and investing whether the market is going up, down or sideways. “Buy low and sell high” does not mean that investors must time the market perfectly. Ideally – we ignore market timing completely – after all, we are investors, not traders. To us, “buy low and sell high” means “reduce risk after periods of good returns and buy into more stocks as the market drops.”

Too often, investors look for the next big investment or protection at the wrong times, rather than seeking out the proper team that can keep you focused on your long-term goals.