Yes, it is true, markets are forward looking, and economic data are backwards looking. But clearly the recent divergence between investor bullish sentiment and the realities for the average American can be considered perplexing.

Market activity suggest investors see daylight at the end of this dark tunnel while a record 20 million Americans lost their jobs in the month of April. Many states are reopening slowly providing hope the economy will “snap back” and lost jobs will be restored. As stewards of your money, we are tired of hearing “…the market knows the job losses are self-inflicted due to shelter in place conditions”. What we know is: the market began 2020 with low inflation, high valuations, high earnings per share and high profit margin expectations, but now there is little visibility with respect to near term earnings estimates. We also know current unemployment rates are at levels experienced during the Great Depression and above levels following the end of WW2. And we can gleam from history, attempts to predict sustainable “snapbacks” then were elusive, as we expect could be the case today.

Yes, the Federal Reserve and Government acted quickly, slashing rates to zero and creating multitrillion dollar rescue packages seemingly overnight. These actions have clearly given investors hope. Famed 1980’s investment manager and author, Martin Zweig is credited with coining the wall street adage: “Don’t Fight the Fed”, which translates to: when the Fed is lowering the cost of money and increasing liquidity, invest, and when the conditions reverse, reduce your investments. This adage has some tried and true validity and has given comfort to many as they have jumped back into the market.

The SP 500 is only down low double digits for the year as of this writing and the tech heavy Nasdaq 100 is down only 5% from its all-time high. So, investing with the Fed on your side has proved profitable once again. But are these market cap weighted indices telling the whole story? Could the average stock performance and average American not be as disconnected as we think? And if so, it could raise very significant considerations for investors and their current mix of investments.

Stock performance as measured by an equal weight S&P 500 index or small cap index paint a much different picture, one where year-to-date losses are at least more attuned to lagging economic indicators. Once we filter out for some of the cash rich or tech dominated names that can survive and prosper in this current environment, you discover many stocks remain down as much as 50% or greater for the year – some with valid business model and/or liquidity concerns.

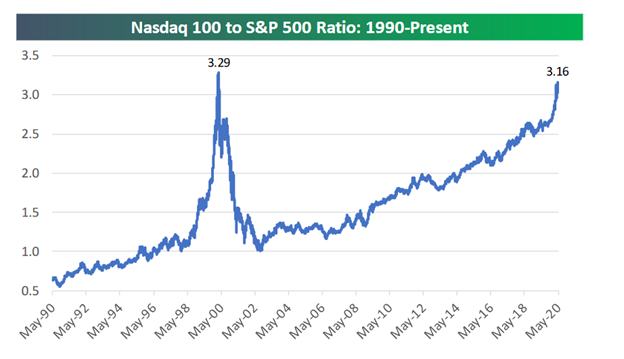

Yes, we believe there is less of a disconnect between Wall Street and Main Street than meets the eye. However, there is a rather significant divergence between cash rich, tech-oriented stocks and the average large or small cap stock. On May 8th, 2020, the Bespoke Investment Group published the below chart indicating the ratio of the Nasdaq 100 to SP 500 indices is nearing the peak ratio recorded at the top of the Dot-Com era. Now, with perfect hindsight, the extreme valuations (and subjectively the euphoria) in late 1999 appears different to us than the strong balance sheet, strong mission, tech-oriented companies of today. But nevertheless, we find it an interesting observation. A small handful of large cap stocks have propelled market cap weighted indices higher. Investors need to judge the sustainability of these stocks vs the opportunity set of all other stocks.

Many company earnings will one day normalize. The Fed will even one day raise rates again. Inflation will even rear its ugly head again, perhaps to the surprise of many as this excess liquidity and simultaneous expansion of debt may come at a cost. Our approach to portfolio construction will take into consideration a 2021 economic revival-though far from guaranteed. In addition, we will analyze and attempt to capitalize on valuation levels and market dislocations and maintain a risk profile that measures up to your unique goals and objectives.

Should you have any questions on our commentary, or approach to your portfolio, please do not hesitate to reach out to us. We hope you and your family are well and safe, and we look forward to a more normalized world.