in the wall of worry, perhaps the higher number of opportunities are being created. Below we list some of these concerns:

- Slowing global growth

- Concerns around Fed policy

- Government shutdown

- US- China changing relationship

- Brexit

- Italian budget standoff

- Fears of recession

- Peak earnings; margins

- Expanding deficits

- Increasing labor costs

- Negative wealth effect

- Elevated volatility

- And the list goes on…

While these concerns do pose a risk and should not be ignored, valuations (see further commentary below) seem to have overshot on the downside and are pricing an environment with no growth. The reality is, our economy continues growing and we do not see evidence of a pending recession in the next 6-12 months.

Companies’ earnings are still rising, albeit at a slower (but not flat or negative) pace than last year. Initial Q4 2018 GDP estimates are between 2-3% and Q1 2019 GDP should remain positive even with an extended Government shutdown lingering.

A Change in Investor Sentiment

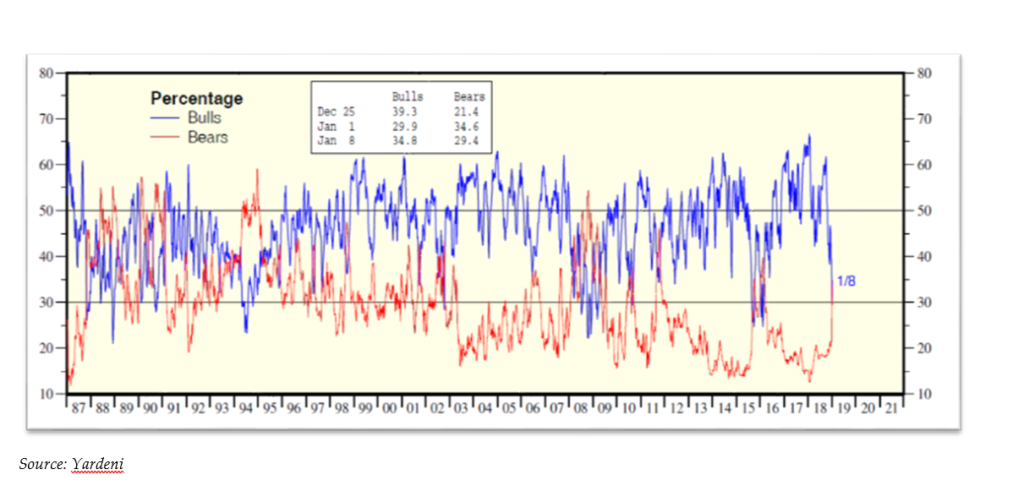

As we wrote in our previous commentary, extreme bullish investor sentiment and expectations were a concern to us and indicative of “a market that may need to reset expectations and valuations”. The intense selling that took place during December accomplished just that. While unsettling for investors, pullbacks such as we saw last month can present opportunities as good, solid companies are caught up in the selling. As the chart below illustrates, there was a significant spike in the percentage of bearish investors and valuations went from highly valued to moderately priced. We view the pullback that occurred as a severe but most likely not a sustainable correction and unlikely the beginning of a more prolonger and protruded bear market, absent a recession.

Less Froth, More Value

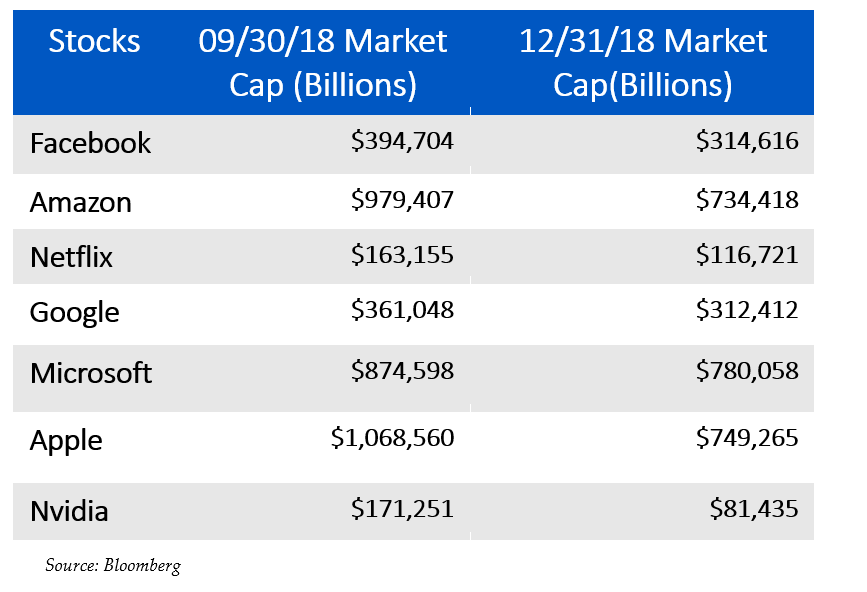

As we wrote about in our two previous quarterly letters, a handful of technology and consumer communications services stocks dubbed FANGMAN were the market darlings for a majority of 2018, until they were not. As the table below depicts almost one trillion dollars of collective market cap evaporated into thin air during the last quarter of the year.

In our view, the mini tech-wreck is a positive development for the long-term health of equity markets. As we enter 2019 some of the excesses in the stock market have been removed and opportunities have been created.

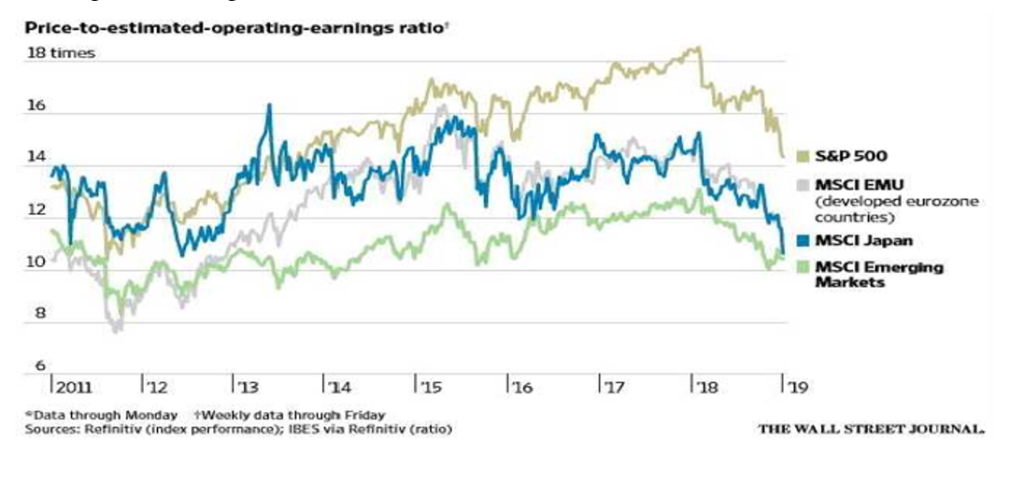

The Q4 selloff in stocks has resulted in lower valuations for most major asset classes globally [see chart below]. In the United States, the S&P500 index is now trading for about 14 times forward earnings; below its 25- year average of 16.2 times. If Facebook, Amazon, Netflix, Google and Microsoft are removed due to their premium valuations [although those have come down too] then the P/E for the index enters a 10-12 times 2019 earnings range, which could portend an attractive entry point for the long-term investors.

Looking under the proverbial “hood of the stock market”, we can find many S&P 500 companies trading for single digit multiples, something that was last evident during the Great Recession in 2008. International markets, both developed and emerging, are also trading below their long-term averages. As Warren Buffet mentor, Benjamin Graham was fond of saying “…market panics can create great prices for good companies and good prices for great companies.” We couldn’t agree more.

Cautiously Optimistic

Given all these factors, we are cautiously optimistic that 2019 could be a better year for the markets than 2018. With investor sentiment remaining too negative, valuations suppressed and low probability of a recession this year, we think equities may continue to build on the comeback off the Christmas Eve lows.

As always, we welcome your questions and comments. Should there be significant changes in your life or a desire to discuss any topic please do not hesitate to reach out to us.