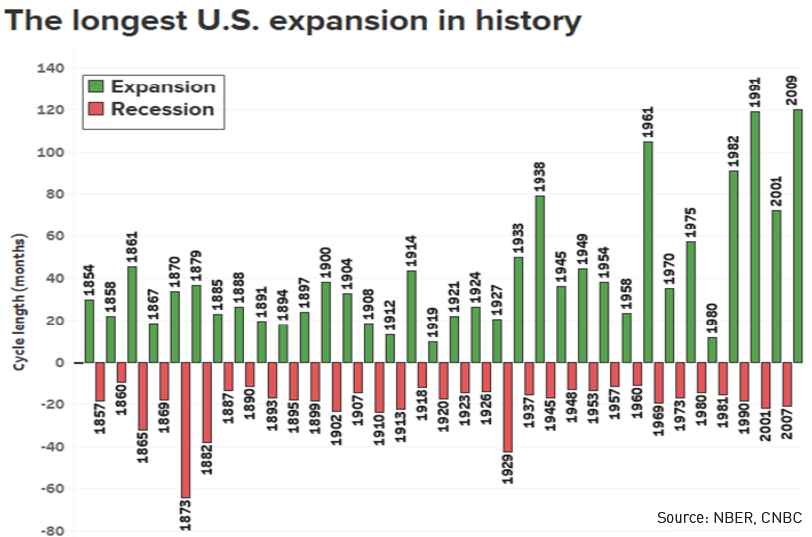

The current recovery started in June 2009 and has surpassed the previous record of 120 months set from March 1991 to March 2001.

While this recovery is now in the books as the longest since the recording of business cycles began in 1854, both the economy’s average annual growth rate and the typical worker’s earning gains have been more moderate than other expansions, which perhaps has extended its longevity. Economic growth has averaged 2.3% per year since June 2009, lower than the average 2.7% growth rate experienced since 1969. In this letter, we look back at the past 10 years and address how this historic decade has impacted today’s markets along with what the next decade may bring.

We expect it could be very different.

THE PREVIOUS TEN YEAR (2009 – 2019)

A condensed look back

Beginning in 2008 with the bursting of the housing market and the unwinding of excessive institutional and individual leverage the US economy teetered on the brink of collapse. The Federal Reserve Board’s primary response was to drive down the cost of money and create a “risk-on” environment, effectively pushing investors out the risk spectrum. The Fed’s interest rate policy of “lower for longer” created the perfect setting for “conventional investing”; purchase any stock, at any price and don’t look back. The Fed’s mission to help companies and markets right themselves became known as “The Fed Put”. In the latter part of this turbulent ten-year span, US investors developed a “home bias” for stocks, with an emphasis on large cap growth-oriented companies. Globally, non-US investors preferred the perceived safety of the American financial system to their own.

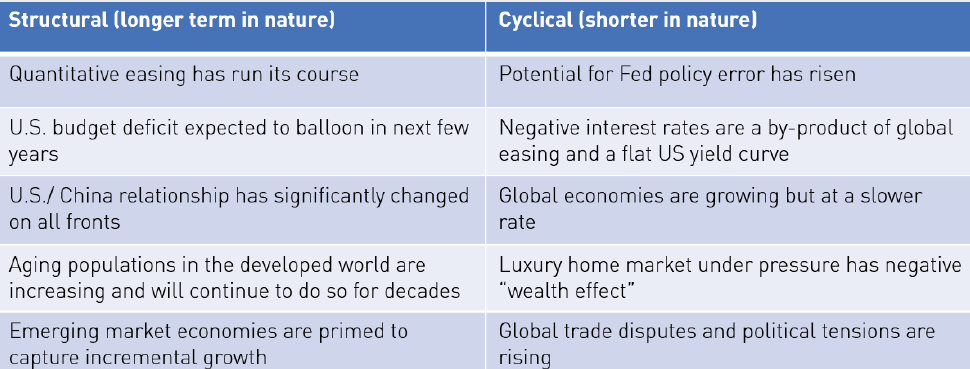

Today we see significant structural and cyclical differences (and some similarities) vs the prior ten years:

As we look forward, we anticipate multi-year returns from “core” US investments to be lower than historical averages. As expectations for future market conditions shift, there is a greater need for unconventional thinking and intelligent portfolio construction. Global investments, investments with a moderate to low correlation to US large company stocks may prove beneficial in the next market cycle.

A TALE OF TWO MARKETS

During the second quarter, markets were driven by the ebb and flow of trade related headlines and comments from the Federal Reserve. The net effect was bond yields declined and US equity markets reached new highs.

The US 10-year Treasury yield decreased 40 basis points (a basis point is one hundredth of one percent) during the quarter to end at 2%. This significant drop in yields reflects concerns about slowing economic growth and/ or expectations for rate cuts. Based on current Treasury yields, one would think that the US economy is seriously weak. However, the S&P 500 is recording new highs, indicating either a confidence in continued economic expansion or an overly bullish market sentiment. We realize that we live in a world where a threat, tweet or unanticipated event can significantly impact markets, however we don’t believe that a recession or valuation correction is a near term concern for equity participants.

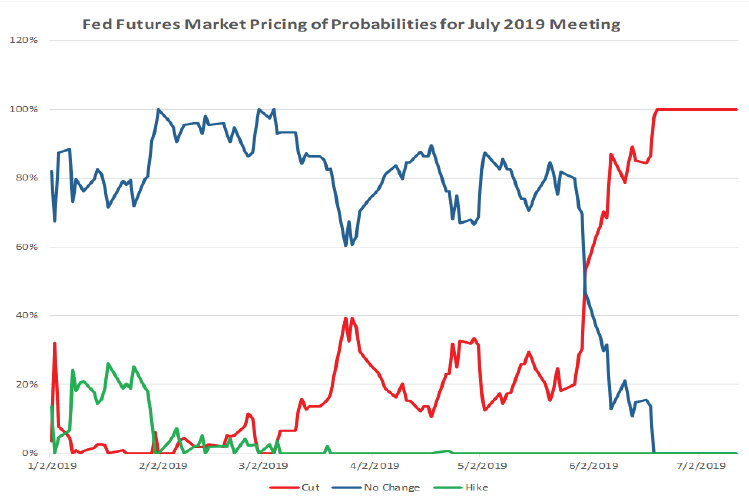

Investors are especially attuned to the level of interest rates and to the Federal Reserve’s next move. The prevailing view (priced into the futures market) is that there will be a rate cut announced during the next meeting at the end of July. We agree. June’s surprisingly strong employment report of 224,000 jobs added to the economy tempered expectations for a 50 basis point rate cut as some had expected, but a 25 basis point rate cut remains firmly on the table.

Source: CME Group Fed Watch Tool

The ongoing trade tensions, potential for Fed policy errors, and decreasing corporate profits are all legitimate worries that could derail the expansion and prove bond investors right. Moreover, the longer a flat yield curve persists with 2 Year notes yielding similar to 10 Yr. notes, the more it bears watching. Elevated trade uncertainty is not only impacting government bond yields globally, but is also depressing business confidence and international trade during a time where global profit growth is already slowing. Managements appear reluctant to make incremental investments beyond those that improve productivity.

A rebound in the global economy later this year, which would be a surprise to many economists, could be the result of Chinese economic stimulus, additional global central bank easing (including the Federal Reserve and the European Central Bank) or a positive resolution to trade disputes; all of which would favor equity investors.

The world remains complicated and interconnected. However, maintaining a long-term vision for investing and an appropriate allocation to financial assets will help tremendously in achieving your goals. Should there be any significant changes in your life or a desire to discuss any topic, please do not hesitate to reach out to us.

Enjoy your summer. As always, we welcome your questions and comments.