A STRONG REBOUND

Risk appetite has returned. The markets had their best quarter since 2009 as optimism with US-China trade talks and a noticeably more dovish Federal Reserve took center stage. Equity and credit markets around the globe erased the declines recorded in 2018.

Source: Bloomberg

The recovery suggests investors viewed the sell-off, more precisely the fourth quarter decline, as a buying opportunity rather than a sign the US was heading into a recession. The Fed “GDP Now” estimates for first quarter GDP have risen from a paltry 0.4% growth to more optimistic 2.0% growth rate as better than expected data has rolled in. Global equities have sharply rebounded, and market valuations are now close to levels recorded at the end of September. Interesting to note, talk of a Fed bent on raising rates has dissipated and there is a growing belief the new direction for the Fed Funds rate is down, not up (more on this idea later).

Source: JP Morgan

Despite the market optimism, there are many uncertainties and unresolved geopolitical issues. While markets like to “climb a wall of worry” -we believe there are real concerns remaining. Some of these concerns include lowered earnings growth rates, a global deceleration in growth, Brexit, trade disputes, China slowing, a rise of populism, and a renewed debate on socialism vs capitalism.

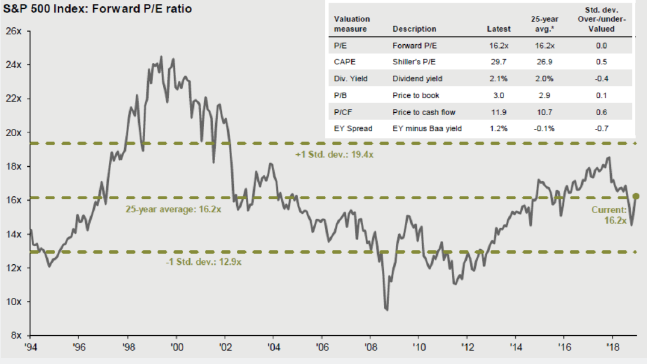

The US economy and corporate profits remain generally solid, but earnings and GDP growth are expected to slow as the effects of the tax cuts begin to fade. As depicted above, stock market valuation levels are hovering around their 25-year averages, with inflation and interest rates not viewed as threats at this point.

THE DOVISH TONE

The minutes from the Federal Reserve March meeting had a noticeably more dovish tone. The Federal Reserve removed two anticipated rate hikes for 2019 and suggested that rates may be on hold for many months. While this might seem like the Federal Reserve is bowing to external pressures, such shifts in policy are not unprecedented and should be viewed as a response to changes in the underlying economic data which notably became more negative in the fourth quarter of 2018. Federal Reserve Charmain Powell cited mild inflation, a sharp pullback in financial markets and clear issues on US growth as reasons for their pause.

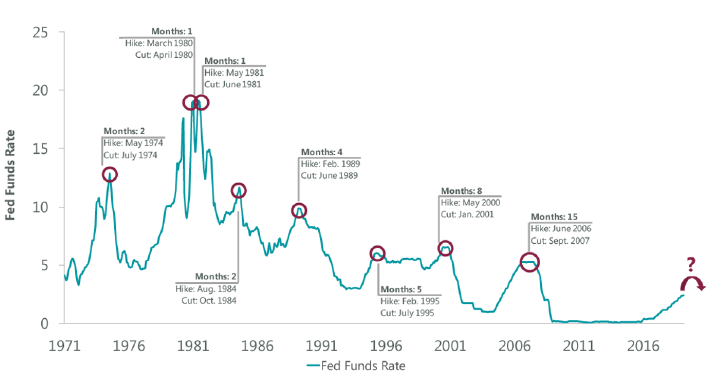

The chart below depicts the time it has taken the Federal Reserve to cut rates after a tightening cycle, going back to 1971. In most cases, the first cut has tended to occur less than five months after the final hike. While we do not know if the December hike will have been the last for this cycle, it seems like the Fed is on a “wait and see” mode for the time being, and expectations price in a high probability for a rate cut in the future. Very few times has the Fed has successfully prevented a recession, but investors are hopeful that easier monetary conditions could be a tailwind for stock prices and economic growth.

Source: Clearbridge, Factset

A BRIEF YIELD INVERSION

In our recent blog post titled: “Yield Curve Inversion – Some Interesting Facts”, we discussed how an important section of the yield curve inverted for the first time since 2007. The 10-Yr Treasury yield fell to a level lower than the 3-month Treasury, sparking renewed concerns about a recession and downward pressure in stocks. It should be reinforced that the yield curve only inverted for about a week before steepening slightly.

While an inverted yield curve has historically preceded the last seven recessions, not every yield curve inversion has been followed by a recession. Moreover, historically, stock market performance continues to be positive following a yield curve inversion.

Source: Bloomberg

THE SOCIALISM VS CAPITALISM CONVERSATION

As a final thought we wanted to touch upon a growing concern regarding economic inequality that seems to have morphed into a “socialism vs capitalism†debate. Eye opening statements such as “the wealth of the top 1 percent of the population is now more than the bottom 90 percent of the population combined†from Ray Dalio and Jamie Dimon’s comment “Socialism inevitably produces stagnation, corruption and often worse†made for hot news headlines. We all know isolated statistics and quotes may not always paint an accurate picture. However, there is no doubt that more can and should be done/debated in the areas of public education, pay and gender equality, executive compensation, taxation and much more. Perhaps less government intervention and less party line politics can be part of the solution. A recently floated idea that Congress should set terms on how, and if, healthy and secure companies should allocate their own capital structure to be “more responsible†seems somewhat naïve, but we look forward to hearing details. We would add that companies that pay attention to social, environmental and governance issues tend to perform well. The larger economic inequality conversation can prove healthy and everyone should hope for sensible deliverables not just public grandstanding and headline grabbing quotes.

We would like to wish a Happy Spring to all of you. Our Northern and Mid-Atlantic clients are especially happy to see the arrival of spring flowers and warm weather. To those in Florida, California and warm weather states you may want to think about visiting us at this beautiful time! As always, we welcome your questions and comments. Should there be significant changes in your life or a desire to discuss any topic please do not hesitate to reach out to us. Warm regards from Withum Wealth Management