The Quarter in Review

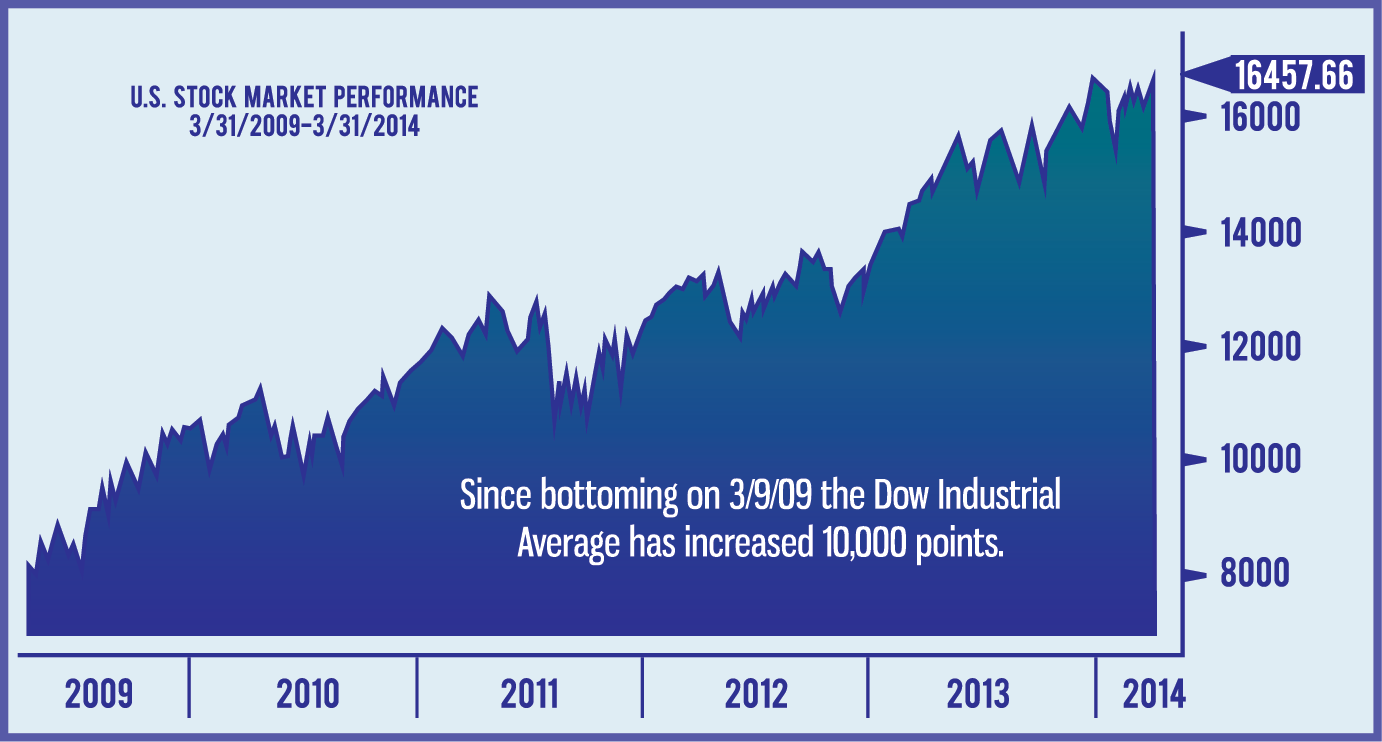

US Bull Market Intact

By early February the US stock market had declined 6% but quickly recovered. As the market marched higher, the pullback became a distant memory. The market continued to ride on the view that jobs are being added to the economy (albeit at a slow pace), inflation is low, 4th quarter corporate earnings were better than forecasted, and, if all else failed, the Federal Reserve would remain accommodative.

In general, with the exception of momentary concerns, investors chose not to be troubled by geopolitical issues and mixed economic reports. By the middle of March the bull market officially entered its sixth year, which is approximately the average duration of US bull markets since the 1930’s.

Download a PDF version of the Investment Outlook »

For the quarter, the S&P 500 was up 1.8% while the Dow was down 0.15%. The international markets were virtually unchanged with the FTSE All World Index up 0.57%. The MSCI Emerging Market Index ended down just 0.54% after rebounding from a 5.5% decline earlier in the quarter. The volatility in the global markets partially reflected investor concerns about the Chinese economy, Federal Reserve tapering, and an overall decreasing demand for commodities. Bond investors fared a bit better. The Barclay’s US Aggregate Fixed Income Index was up 1.8% indicating that longer-term interest rates, in general, had migrated down during the quarter.

Source: Bloomberg

U.S. Economy

The Taper is Likely to Continue, Fed is Slightly More Aggressive?

In her first post FOMC press conference as Federal Reserve Chair, Janet Yellen announced that the Fed would again reduce long-term bond purchases by $10B in April, bringing the monthly total to $55B (down from the peak of $85B). The measured step reduction in asset purchases should continue as long as there is sufficient underlying strength in the economy to support improvement in job creation. While this was expected, the bond and stock markets were temporarily spooked as the Federal Reserve abandoned its original target unemployment rate; and will now focus on a broad spectrum of economic indicators as a gauge for future tapering. Yellen’s most impactful comments related to an actual time frame for an increase in interest rates. Specifically, the new Fed Chair stated the Federal Reserve is likely to begin raising rates about six months after the end of its bond purchases. This, coupled with 2015 rate hike forecasts by a majority of FOMC participants, led to a quick spike in interest rates and drop in the stock market as investors believed this represented a slightly more aggressive outlook on interest rate hikes. While the Federal Reserve’s taper of its monthly bond buying has not resulted in an increase in the 10 Year Treasury yield (which ended the quarter at 2.7% vs. 3.0% at year-end), the taper, as well as Yellen’s comments, has resulted in an increase in shorter Treasury yields, thus slightly flattening the yield curve.

Economic Indicators Suggest Slow Growth Continues

On March 26th the Commerce Department announced that GDP grew at a 2.6% annual rate in the fourth quarter of 2013 down from 4.1% in the third quarter. The slowdown in growth was mostly attributable to cuts in local and federal spending due to the 16-day government shutdown in October. Economic data in the first quarter were mixed, but on balance confirm that the economy is growing slowing. As with all economic statistics announced throughout the quarter, it was difficult to decipher the degree to which unusually frigid weather affected the outcomes. Throughout the quarter, inflation remained below the Federal Reserve’s target rate of 2%.

International

Economic Overview

We continue to foresee a strengthening global economy that is somewhat blurred by geopolitical headline news. The evolving situation in the Ukraine remains a concern, particularly if President Putin changes his tune and indicates an interest in absorbing other regions of the Ukraine, and stronger reciprocal economic sanctions are imposed by the US and Russia. Any sanctions that would disrupt exports of energy from Russia could lead to higher global oil and natural gas prices, thereby negatively affecting economies worldwide and derailing Europe’s recovery.

Investors remain concerned about slowing growth in the Chinese economy. Perhaps the most important threat to China’s economy, however, is its shadow banking system. These unregulated banks have become the prime source of lending to small and mid-sized companies that have been unable to get funding from traditional banks. As China attempts to rein in its burgeoning money supply by tightening credit, this could increase the number of defaults of shadow banking loans and have a negative impact on the Chinese financial system. From a collective perspective, emerging markets have become relatively more attractive from a valuation standpoint and we continue to monitor them closely.

A Look Ahead

What the Facts Suggest for the

Balance of 2014

There are many reasons to believe that the dollar will strengthen over time. The US has the healthiest growth prospects of the world’s developed economies, with the possible exception of the UK. The US also has a shrinking current account deficit that is at the lowest level in 14 years. The Federal Reserve has indicated its intention to raise rates, while the European Central Bank is still talking about accommodative monetary policy and the People’s Bank of China is keeping the Yuan at its lowest level in 12 months. All of the above suggest that it would not be surprising to see the U.S. dollar appreciate somewhat later in the year.

Some analysts contend that renewed interests in equities by retail investors, and a low level of market fear, are precursors of a market reversal. If that is true, then the 2013 inflow of assets into equity mutual funds of $194.4 billion, the largest since 1992, may suggest we are in the later stages of a bull market. Add to this the fact that the Chicago Board of Options Exchange Volatility Index (VIX), a widely used measure of “investor fear”, has remained low throughout 2013 and 2014. For example, the VIX reached levels above 20 only 3 times in 2013 and once so far in 2014. Compare this to 2008 and 2009 when the VIX was above 20 for 223 and 247 days, respectively. These two facts, however, must be considered in the context of the unique circumstances of today’s markets. For example, the recent significant inflows into equities could be the result of investors’ desire for the yield they cannot find in high quality fixed income investments. Similarly, investors’ complacency may be more an acceptance that dividend paying stocks seem to offer a better risk/reward than bonds. As rates migrate higher it is a certainty that fixed income prices will be negatively impacted. Stocks, on the other hand, have a chance to go higher even if rates rise, particularly if this increase is based on improved economic activity.

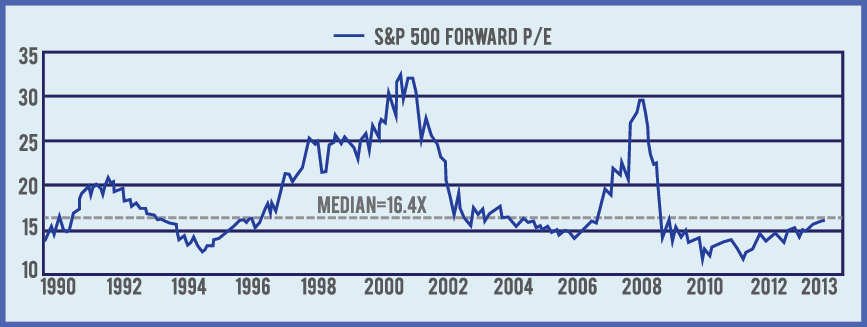

As we stated in our 4th quarter 2013 letter, it is important to note that the valuation story in the US is not as compelling as it has been in past years. While we do not believe multiple expansion will be as pronounced in 2014 as it was in 2013, there still appears to be some room for price-to-earnings (P/E) growth. For example, the current S&P 500 P/E based on forward 12 months earnings is still well below recent market peaks (as seen in the S&P 500 Forward P/E graph). In addition, it is possible that the very temperate growth we have had coming out of the Great Recession, versus the quicker and more robust growth of more typical recoveries, could help to prolong the market’s advance. While we have an overall positive outlook on the US economy in 2014, it is likely that returns will not be as robust as they were last year.

Important Disclosure: Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by PWM Advisory Group. [“PWM”] ), or any non-investment related content, made reference to directly or indirectly in this newsletter will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this newsletter serves as the receipt of, or as a substitute for, personalized investment advice from PWM. Please remember to contact PWM in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services. PWM is neither a law firm nor a certified public accounting firm and no portion of the newsletter content should be construed as legal or accounting advice. A copy of the PWM current written disclosure statement discussing our advisory services and fees is available for review upon request. Photo Credit: tpsdave

If You Liked This Article, SHARE IT!

Help Us Spread The Word. Share This Article With Your Friends & Peers