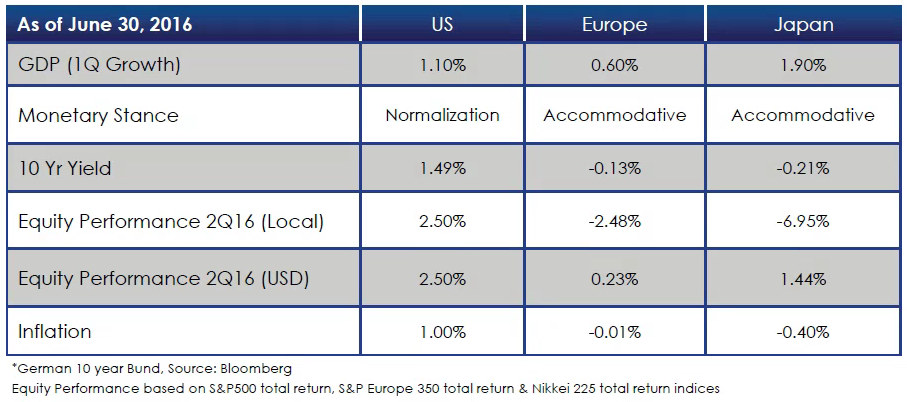

The Quarter in Numbers

The Negative Interest Rate World We Live In

Several Central Banks around the world have ventured into the once-unchartered territory of negative interest rates. Given the previously unthinkable ultra-low (or negative) interest rate world we live in, we want to devote generous space to review negative interest rates.

Let’s begin with defining a negative interest rate. In a “normal” interest rate environment, a borrower will pay an interest rate to a lender in return for a loan. When negative interest rates are in place, this order is reversed; the lender pays the borrower. Basically, you are paying an interest rate for lending funds. Let’s look at a real life example, the German 10 year Bund, which as of June 30th yielded -0.13%. An investor who lends money to the German government (buys a German 10 year Bund) is paying 0.13% for the “privilege” of lending money to the German Government. Because interest rates are negative, this investor will lose money in real and nominal terms each and every year for ten years.

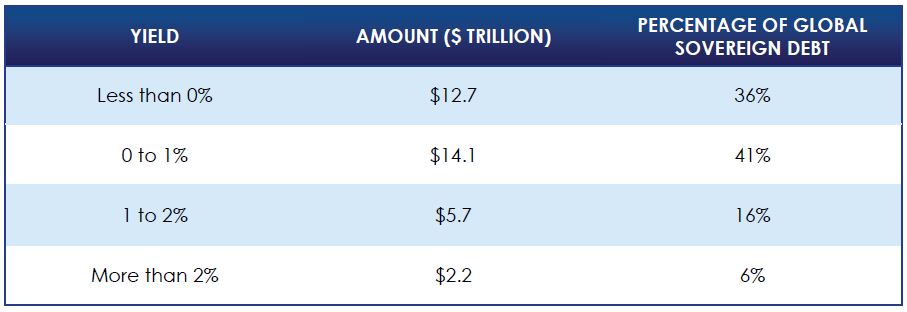

To put this into context, consider the $35 trillion sovereign global debt market as of June 30th, 2016. As the following chart depicts, 36% of sovereign bonds around the world have negative interest rates. Furthermore, 94% of global sovereign debt yields less than 2%!

Distribution of Global Sovereign Debt Yield

Source: Bloomberg/ Bianco Research

Why would Central Banks Push Interest Rates into Negative Territory and how do they Influence Interest Rates?

Central Banks have resorted to negative interest rates in an effort to spur bank lending and stimulate the economy. They control the overnight rate, which is the rate that commercial banks (borrowing institutions) typically receive (but now sometimes pay) for overnight deposits.

In Japan and the Eurozone the deposit rate has turned negative. By making commercial banks pay for deposits held at the Central Bank, the intention is to incentivize banks to make more loans to consumers instead of parking idle funds in reserves. Central Banks theorize a negative interest rate will push down short term rates on other types of lending such as mortgages and consumer rates thus further spurring investment. This in theory provides an economic boost and weakens the currency of any participating economy, thus boosting manufacturing and benefitting exporters.

Now Consider Government Bonds.

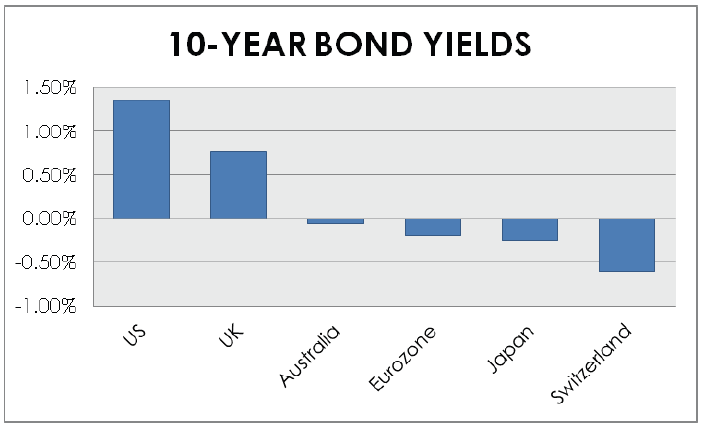

Government Bond buying programs in Europe and Japan (quantitative easing), expectations of slower global growth and a search for safe haven assets are also factors influencing the current yield environment. Ten-Year government bonds of Switzerland, Denmark, Finland, Japan and Germany to name a few have negative yields. In the United States, the yield of the 10-year Treasury is still positive at 1.38%. This may not sound very attractive but once the alternatives are considered it becomes one of the best, if not the best, option for global bond investors. This environment of low and negative interest rates around the world has served to drive down yields for the US bond market.

It will be difficult to predict when the US bond market decouples from the gravitational pull of negative yields across the globe. Traditional economic theory suggests that nominal interest rates are “zero bound,” and can’t stay in negative territory for long because savers and investors will withdraw their cash and store it themselves, emptying banks and crippling the financial system. This assumption has now been challenged. While we have learned investors and/or depositors are willing to pay a price for the presumed safety of their funds, the long term implications of negative interest rates are yet to be fully understood. What is certain is that economic textbooks are being rewritten and only time will determine the impact of this negative yield environment on the real economy.

The Brexit Vote is Official. What Next?

As we wrote in our special update, 52% of British citizens who participated in the referendum voted to leave the European Union (EU). Both the surprise outcome and the uncertainty relating to how the exit would unfold, contributed to a large decline in global markets and a shift toward safe haven assets such as the dollar, US Treasuries and gold. The Sterling fell to a 30 year low against the dollar, the 10-Year US Treasury yield traded down to nearly a 1.4% yield and gold jumped almost 5%. Most global markets staged a dramatic comeback, however, as fears over another Lehman-type shock started to subside and Central Bankers around the world indicated they stand ready to provide liquidity to the market. The post Brexit vote market dip and subsequent comeback served as yet another reminder to investors why it is important not to overreact to short-term market swings.

Bear in mind that the UK will not be leaving the European Union overnight. It is a process that will take place through a multitude of negotiations over a number of years. While it is highly unlikely, it is even possible that the UK will stay in the European Union. We expect political events and change will unfold over the next several years adding pressure to the European Union structure and the cohesion within it. We believe that the EU will take a fairly hard negotiating stance during the exit process in an effort to avoid setting a precedent. It is important to note that citizens of France, Italy and the Netherlands have begun to call for their own referendums to leave or remain in the European Union.

What is the Impact of Brexit to the US Economy?

In the United States, recession odds remain fairly low although they are higher than before the Brexit shock. The economy is currently growing at a rate of 2-2.5% and UK challenges should have little direct impact to US growth (US exports are not highly dependent on the UK). Over the past few months, the labor market has continued to tighten as evidenced by the reduced trend in jobless claims and increase in wage growth. This in turn is bolstering the US consumer; retail sales are rising, and the housing market continues to inch forward.

The Federal Reserve will likely take a more cautious stance and a July rate hike is unlikely. In addition, long term policy goals may now take more time to unfold as we anticipate interest rates to be lower for longer.

Will the Dollar Appreciate?

The risk-off trade environment that ensued after the Brexit vote resulted in, and will likely continue to support, strength in the dollar. A powerful rally in the dollar could have a ripple effect globally. For example, a surging dollar presents a headwind to the earnings of US multinationals and hurts U.S exporters and manufacturers. It also has negative implications for the price of oil which is quoted in dollars. As we have seen, cheaper oil has some positive benefits, but extremely cheap oil leads to a host of negative issues within the energy related businesses (layoffs in the industry, increased likelihood of defaults on the debt of highly leveraged energy companies, etc.) In addition, commodity oriented emerging market countries are generally hurt by a rising dollar as it reduces their ability to service their debt.

Where Do We Go From Here?

In the near term, uncertainty will likely cause more volatility and raise the possibility of additional sharp pullbacks, but stocks and bonds will ultimately trade on fundamentals and not headline news. Corporate earnings are likely to improve from the first quarter, but the pace of earnings growth is expected to be modest in light of recent events.

We will continue to focus our investment management efforts on fundamentals while keeping a close eye on any short term dislocations in the market. Whether it be negative rates, political shocks, exogenous events, etc. our ultimate goal remains unchanged; build transparent portfolios that meet your long term needs and objectives. Should you have questions regarding the current economic or political environment and how it may impact your long term plan, please do not hesitate to contact us.