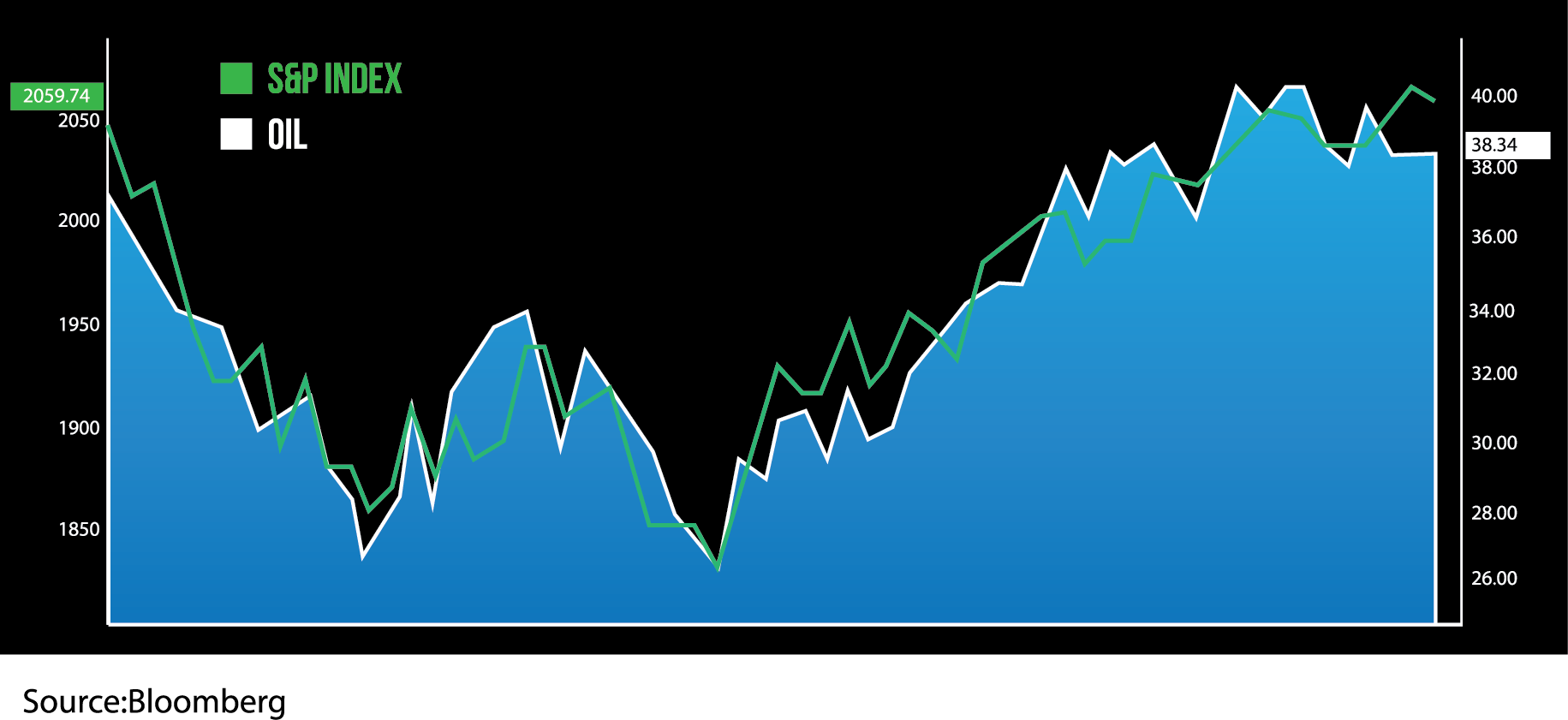

A Roller Coaster Quarter

The first quarter of the year was characterized by elevated volatility, concerns about China, and global recession fears. In addition, equity markets exhibited a much higher correlation to oil prices than in the past. Early in the quarter, oil prices dropped to levels not seen since 2003 which caused global markets to retreat into correction territory. Recovering oil prices, better than expected economic data from the United States and dovish Central bank policies helped ease some of those fears. As a result, most markets staged a dramatic comeback in the latter part of the quarter to erase all 2016 losses. Emerging markets outperformed developed markets, helped by stronger commodity prices, a lower dollar and reduced expectations for US rate increases.

Lessons Worth Repeating

The first quarter of 2016 reinforced several key investment principles that, in our opinion, are central to long-term investment success:

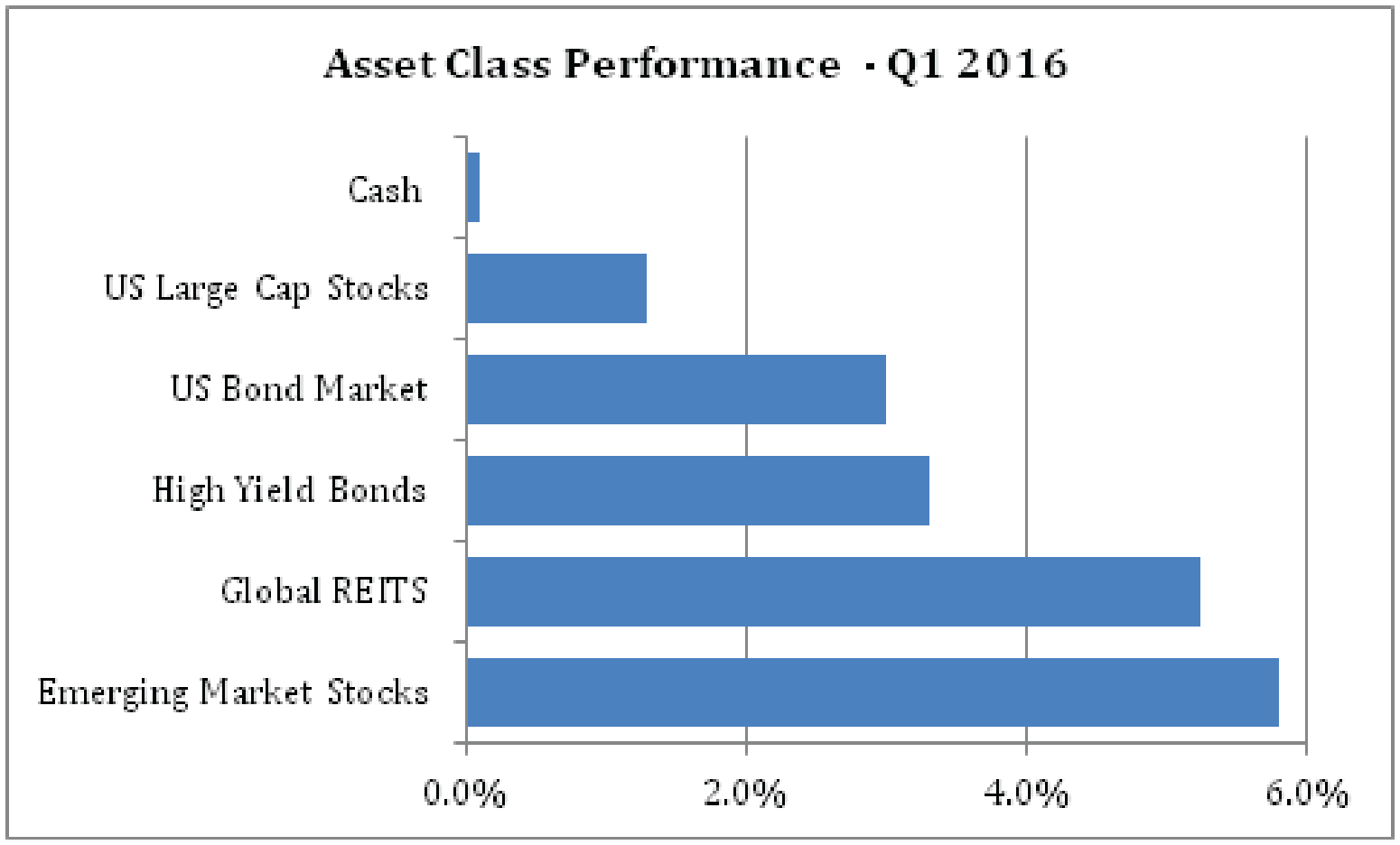

1.Diversification still matters. For the last three years US stocks have outperformed many other asset classes. The first three months of 2016, however, reminded investors that diversification is still important. As we highlight in the chart below, emerging market stocks (5.8%), global REITS (5.3%), and both high yield bonds (3.3%) and the aggregate bond market (3.0%) more than doubled the performance of US large cap stocks (1.3%) in the first quarter.

2. Investors should focus on long-term market trends. Panic selling during volatile times will generally not be productive. US stocks began the year down 10% only to rebound 13% from the year’s market low. While pulling money out of the stock market during a market downturn may feel good at the time, it can be detrimental to achieving your long-term investment goals.

3. Remain true to your plan. It is important for investors to rebalance their portfolios and ensure their holdings properly reflect their long term strategic plan.

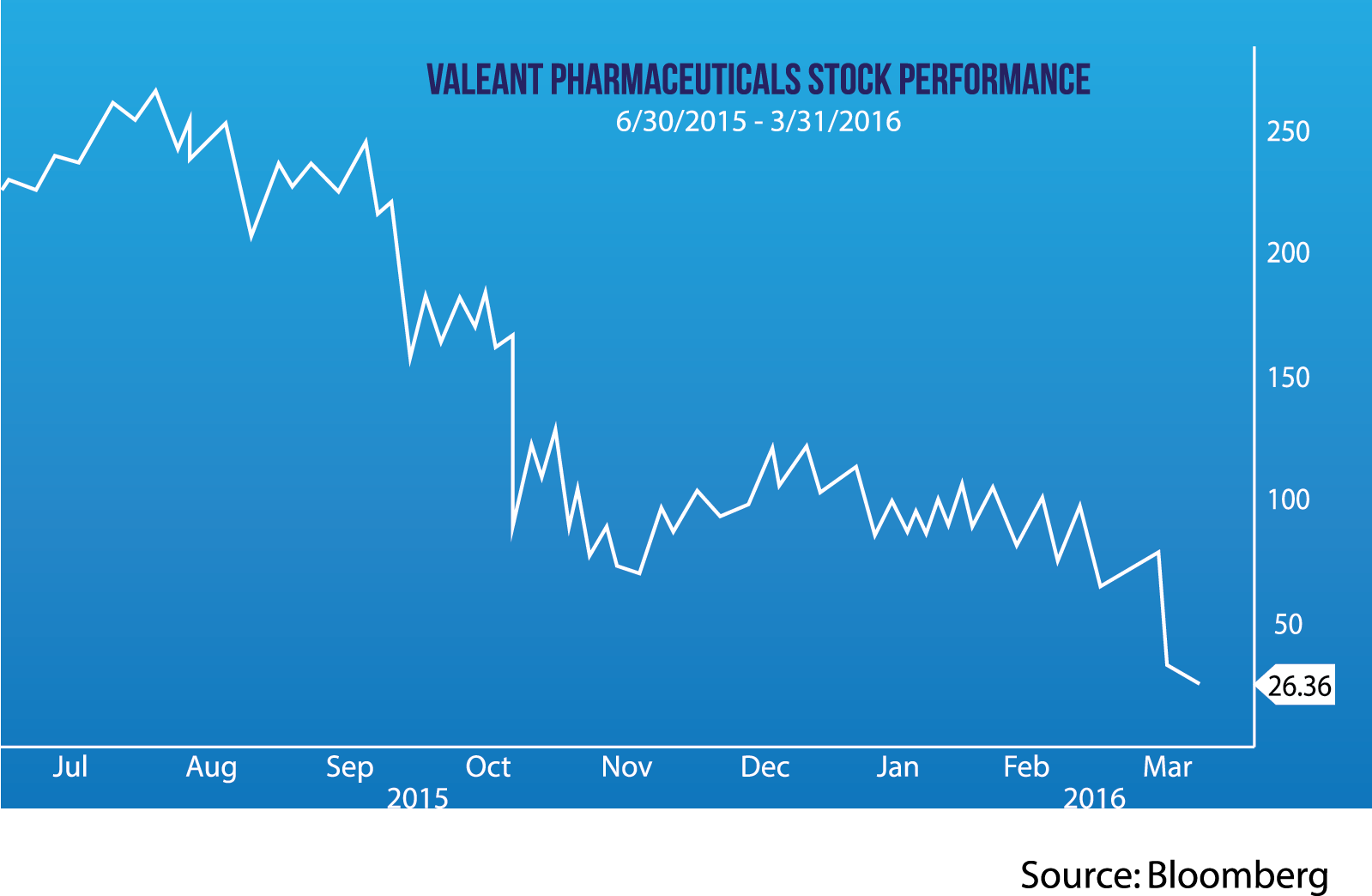

4. Falling in love with any one stock is risky business. Just ask famed investors Robert Goldfarb, head portfolio manager of the Sequoia Fund who is regarded as an “ultimate stock picker” by Morningstar, and Bill Ackman, founder and chief executive officer of Pershing Square Capital Management. Both investors held large stakes in Valeant Pharmaceuticals International Inc through their respective funds. Valeant (ticker symbol: VRX) is a large Canadian healthcare company whose stock exhibited remarkable year-over-year growth up until last summer. Unfortunately for investors in Goldfarb’s and Ackman’s funds, Valeant’s stock has plunged approximately 90% from its high recorded in August 2015 due primarily to concerns over questionable pricing practices and their ability to pay off debt. The collapse of Valeant’s stock price is a sobering reminder of the risks investors bear when concentrating too much of their assets to one company.

A Look Forward

Expectations for the upcoming earnings season remain low but conditions should improve later in the year if the headwinds from the “oil prices down/dollar up” dynamic recede. The US economic backdrop is solidifying, a view that has been reinforced by continued improvements in the labor market. Importantly, recent data suggests more Americans are entering the labor force and wage growth continues to move higher. If these trends continue (stabilization of oil price, a slower pace of dollar strengthening and an improving labor picture) global growth conditions should continue to improve and we would expect the stock market to reflect this optimism. However, should the stock market continue to rise and possible exceed previous highs we would like to see these gains supported by sustainable earnings growth.

The weaker dollar has helped stabilize both commodity prices and emerging market currencies and should provide support for corporate earnings. We remain cautious on recent oil price improvements as they mostly relate to expectations for falling supplies and a production freeze, which have not yet materialized, and continue to look for signs of a long-term stabilization of oil prices. However, if the oil/stocks correlation remains elevated, continued improvement in the stock prices may hinge on the path of oil prices.

While we remain cautiously optimistic about the prospects for global growth, we anticipate continued volatility in equity markets. In the United States, this year’s presidential election and the potential for a Republican brokered convention could also contribute to increasing volatility levels. We advocate a diversified portfolio of assets as the best way to weather market volatility while achieving long-term goals.