What a Quarter…

The third quarter of 2016 witnessed the first OPEC production cut agreement in eight years, record breaking viewership of the first US presidential debate, a prominent hedge fund manager charged with insider trading and rumors that a major German Bank (Deutsche Bank) may be in need of a significant cash infusion. We also learned more about two types of Wells Fargo employees; the good (whistle blowers who were shamefully fired) and the bad (creative staffers who created 2 million fraudulent accounts to game the bonus system).

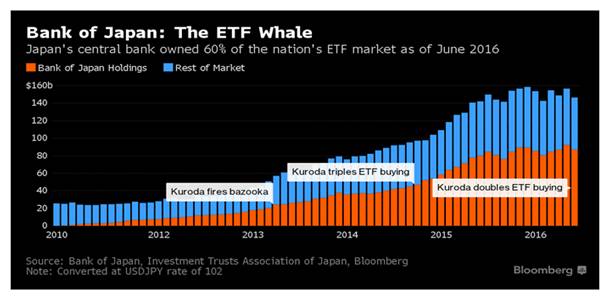

Moving on from banks to central bankers, we heard our Fed Chairperson speaking openly about the possibility of the Fed buying equities in the event of a downturn, something that they are currently legally barred from doing, while in Asia the Bank of Japan already owns 60% of the Japanese ETF market!

Not only is the Bank of Japan becoming the largest shareholder in many companies, it is also now trying a new monetary experiment by targeting a 0% yield in the 10 year Japanese Bond. Given the current low yield environment, it is worth noting that the end of the third quarter marked the 35th anniversary of the record high yield for the US 10 yr Treasury yield (15.84%).

In the United States the labor market continues to improve as evidenced not only by a decrease in the unemployment rate but also in the multi-decade low level of unemployment claims and what seems like the start of higher wage pressures. This tightening of the labor market, combined with a possible sustained firming of energy prices resulting from the OPEC supply cut agreement, and a global movement to nationalism could serve as catalysts for an increase in inflationary pressures.

After an eventful quarter, the last three trading months of the year are upon us. Volatility is expected to remain elevated as there are many key events that could impact the markets: a highly contested US election; the Italian constitutional referendum; continued Brexit planning in the United Kingdom; a strong likelihood of a rate hike by Federal Reserve in December and the seemingly escalating risk of foreign military provocation by rogue nations.

Hedge Funds: SEC Charges and Big Bet Failures

Hedge funds have been in the news lately both because of poor performance and charges of improper trading. Some top managers admitted difficulties with the current environment by announcing fee cuts or even closing their doors. As some prominent hedge fund managers grudgingly have admitted – there’s more hedge funds than taco bells. So many players in the space trying to execute the same strategies can help explain some of the under-performance of these funds.

We expect an industry shakeout is forthcoming.

Not only is the space crowded, it continues to be ripe with scandal. Leon Cooperman, the heretofore well-respected billionaire Omega Advisors hedge fund manager, has been charged with insider trading. He is accused of making $4 million in illegal profits by using nonpublic information related to an energy deal in 2010. Cooperman is now front and center in the hedge fund universe spotlight with a family drama also involving his son and grandson; replacing Bill Ackman and the Valeant saga for the time being.

Bill Ackman’s Pershing Square remains the poster child for high fee, underperforming, and “big bet” hedge funds. The hedge fund fee structure, typically 2.5% plus 20-30% of profits, may in one form or another, influence behavior and result in a swing-for-the-fences mentality. In our view, big bet positioning is not a prudent strategy. In addition to Bill Ackman, many big names in the hedge fund world collectively lost billions by betting on Valeant Pharmaceuticals -underscoring the growing phenomenon of hedge fund groupthink.

Central Bankers Chemistry Lab

Global central bankers are taking unprecedented measures to stimulate their respective economies.

Let’s begin with the Bank of Japan’s (BOJ) quantitative easing program, which analysts at Charles Schwab refer to as Godzilla- sized. The purpose of QE is to increase the monetary base to make more cash available, encouraging lending to drive growth and generate inflation. Said differently, the monetary base is the amount of currency directly supplied to the economy. During September 2016, with the monetary base at 405 trillion yen, the BOJ announced its intent to further expand its monetary base until growth in core inflation overshoots its 2% target. To put the monetary base in Japan into context, it is currently the same size of the monetary base in the United States, even though the US economy is 4 times larger than Japan’s.

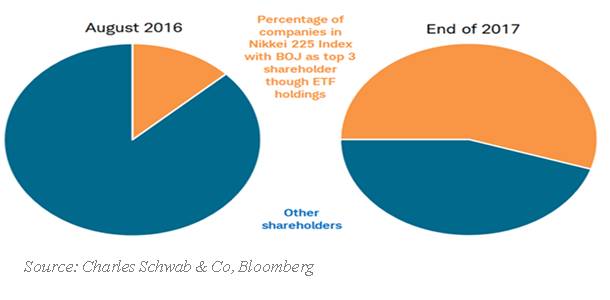

Is there a limit to what they can buy? One third of all Japanese government debt is already owned by the BOJ. At this pace, they could run out of bonds in the not too distant future. This is the main reason the BOJ redesigned its program during September. The goal is to purchase whatever amount is necessary to stabilize longer-term bond yields around zero, rather than buying a fixed amount every month. The hope is for the yield curve to steepen, helping banks and insurance companies. But the buying doesn’t end there- the BOJ is also buying stocks through its ETF purchases! It already owns 60% of the ETF market as of 6/30/2016 and is on track to become the No. 1 shareholder in over 50 companies in the Nikkei 225 by the end of 2017.

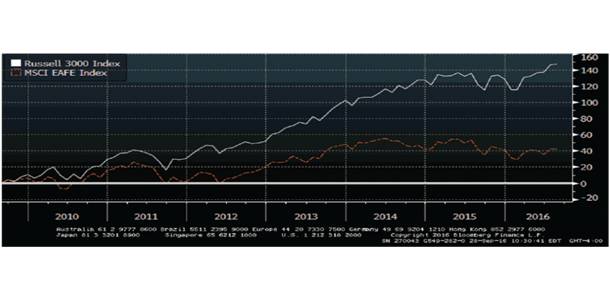

While the BOJ might seem pretty unconventional in their monetary policy, this type of market intervention is hardly unique. The Bank of England unveiled a $13 billion plan to purchase corporate debt on Aug. 4, less than two months after the start of a similar program at the European Central Bank. The US Federal Reserve experiment with QE which began in November 2008 has helped fuel a stock market boom and tremendous relative outperformance versus other international stock markets.

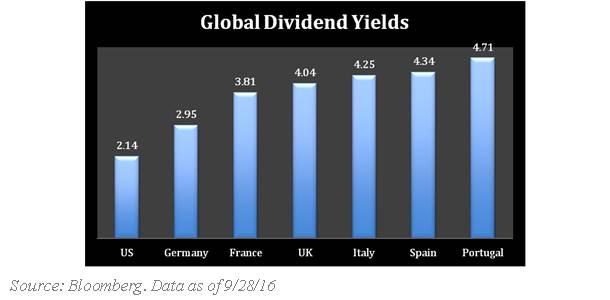

The relative outperformance of the US markets is also observed when comparing the dividend yields of the domestic markets versus those of major developed European markets. Lower yields typically indicate a market that has increased in value and vice versa, all else held equal. As the chart below depicts, the yields are much lower in the domestic markets versus the major developed European markets, which could indicate attractive valuation for European markets on a relative basis.

The central bank chemistry lab apparently does not exclude the Federal Reserve Board. In Janet Yellen’s own words: “ If we found, as I think other countries did, that they could reach the limits in terms of purchasing safe assets like longer term bonds, it could be useful to be able to intervene directly in assets where the prices have a more direct link to spending decisions.” She added that this could help the economy during a downturn and suggested lawmakers consider changing the law to allow for the purchase of these assets. In our view, this would not be advisable and we do not envision Congress passing a law to give the Federal Reserve the power to buy stocks anytime soon.