How do You Create an Income Stream from Your Savings?

At retirement, everything changes. Not only will you have more free time to focus on what you like, your tax situation is also changing. Wages have ended and taxable income has decreased significantly. Furthermore, you are likely to face higher taxes in the future. The reason for that is that once you reach age 72 you will be required to withdraw funds from your tax-deferred accounts each year. By age 70, if you haven’t already begun drawing Social Security, those benefits will increase your taxable income as well.

The first years of retirement may provide a temporary dip in taxes and while it is tempting to enjoy paying no or low taxes for a few years, it may be best to take a different approach. Consider taking some money out of your tax-deferred retirement accounts while you are in a low tax bracket. Not only do you get to pay a low tax rate now, but it also reduces your future required minimum distributions (RMDs) which would be taxed at a higher rate.

How does Tax Smoothing Work?

The key is determining how much to withdraw from your retirement account in order to pay low taxes without going into a higher tax bracket. Tax smoothing means increasing your taxable income just enough to fill in low tax brackets.

As an example, consider this two-year situation:

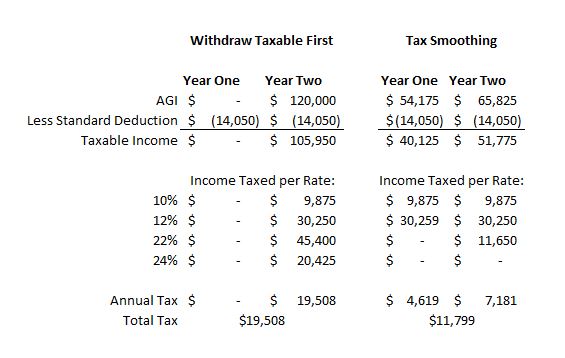

A 67 year-old, single taxpayer has $120,000 in an IRA and $120,000 in a taxable account. The taxable account has no unrealized gains. The plan is to spend $120,000 each year for two years. Under a traditional strategy of taking funds from the taxable account first, the taxpayer would deplete the taxable account in year one and the IRA in year two. In this situation, the taxpayer would owe no tax in year one, but would owe $19,508 in year two. The chart below shows that the first $14,050 of income, representing his standard deduction, is tax free. After that, successive dollars of income are taxed at higher rates. His last dollar of income is taxed at 24%, his marginal tax rate.

If instead he uses a tax smoothing strategy, then he would withdraw enough from his IRA in year one to fill in the 12% tax bracket. This results in a tax of $4,618 in year one and $7,181 in year two. The total tax paid is $11,798, almost 40% less than under the traditional method. The total tax is lower because it takes advantage of the standard deduction in both years and moves income into lower tax brackets.

While this general process is straightforward, the devil can be in the details. The example above does not take into consideration the multi-year nature of retirement or the impact early withdrawals have on future required minimum distributions. In addition, there are several considerations to keep in mind when designing a tax smoothing strategy. These include unintended tax consequences, the impact on Medicare premiums, and the balance of tax type accounts.

Realizing additional income in an otherwise low tax bracket year can cause unintended tax consequences such as capital gains being pushed into higher brackets, the reduction of itemization for medical expenses and/or an increased tax on Social Security income. It is important to pay attention to these items if you fall into any of the following categories:

- Your taxable income is close to a capital gains tax break point. Tax smoothing may increase your tax on qualified dividends and capital gains.

- You itemize deductions and have significant medical expenses. Tax smoothing could reduce your deduction.

- You are already claiming Social Security but the taxable portion is less than 85%. Tax smoothing could increase the taxable portion of that income.

Another issue to pay attention to is Medicare premiums. Premiums increase for taxpayers with high income. The first step-up in premiums occurs around the top of the 12% tax bracket. If your tax smoothing includes realizing income higher than this amount, then you may want to focus on filling income up to one of the Medicare income-related monthly adjustment amount (IRMAA) brackets.

Furthermore, the effectiveness of tax smoothing is influenced by your mix of after-tax investment accounts, pre-tax retirement accounts and non-taxable Roth accounts. The ability to withdraw funds from different accounts is essential to managing taxable income. Balancing your mix of account types is part of the calculation as to which accounts to tap for expenses and how to approach Roth conversions.

Take the time either before you retire or early in the process to assess your situation. The early years of retirement are prime time for tax management strategies—don’t miss this opportunity.

Every investor’s situation is different, please consult with your tax and financial trusted advisors to plan for and implement a similar strategy. They will be glad you asked.