The London Interbank Overnight Rate (LIBOR) has been the world’s most widely used benchmark of short-term rates for decades; however, its significance in the global financial system is slated to officially end in June of 2023. This shouldn’t come as a surprise, as discussions of abandoning LIBOR as a benchmark rate began over a decade ago in 2012. During this time, a series of scandals exposed the flaws inherent in the way LIBOR is calculated, flaws that had allowed banks to manipulate the rate to boost their credibility and profits. These scandals led to significant distrust in the financial industry and spurred a wave of fines, lawsuits, and regulatory actions. In 2021 the body that regulates LIBOR, the UK’s Financial Conduct Authority (FCA), announced that LIBOR would not be available for any new contracts beginning in 2022. The FCA also confirmed that all USD LIBOR tenors would be discontinued following June 30th,2023, and any remaining contracts that reference LIBOR would switch to an alternate rate.1 To understand how we arrived at this point, it’s crucial to understand what LIBOR is and how it’s evolved over time.

A brief history of LIBOR

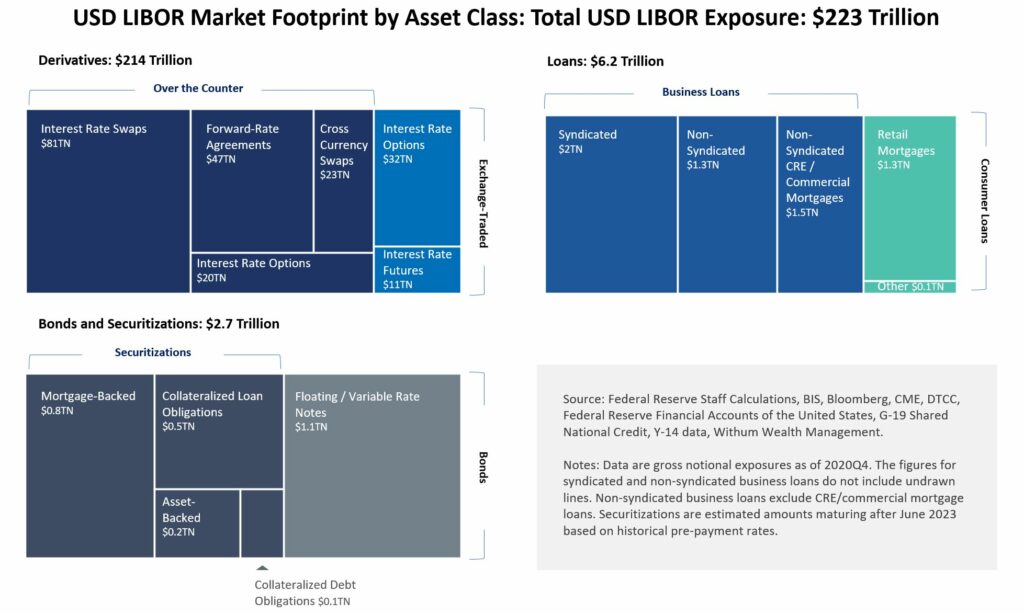

In its most basic form, LIBOR is meant to represent the average rate at which the largest and most creditworthy banks would be willing to borrow from one another on an unsecured basis. It’s based on several different currencies, including the US dollar, the Euro, the Swiss Franc, the British Pound, and the Japanese Yen, and is published with maturities ranging from overnight to 12 months. LIBOR’s roots can be traced back to 1969 when a Greek banker named Minos Zombankais brokered a syndicated loan worth $80m to the Shah of Iran. The rate tied to the loan was a fluctuating interest rate based on the reporting costs of a set of reference banks. Adoption of this kind of variable rate proliferated, and in 1986 the British Banker Association (BBA) officially embraced it by formalizing the data collection and reporting process. By 2021 the size and scale of the LIBOR market had skyrocketed, and more than $230 trillion worth of financial assets were using LIBOR as a reference rate. Derivatives such as Interest Rate Swaps had the largest market share; however, more than $1 trillion in consumer loans such as Mortgages and Student loans also had exposure to LIBOR.2 See the below for a more detailed breakdown of the LIBOR Based Market:

How were banks able to manipulate LIBOR?

LIBOR is calculated based on interest rate submissions from a panel of banks appointed by the Intercontinental Exchange (ICE). The only banks considered for membership on the panel are those with a significant presence in the London market. For example, the USD LIBOR panel includes some of the largest and most financially sound banks, such as Citibank, JPMorgan, and Bank of America. The panel banks report their funding rates to the ICE Benchmark Association every morning. ICE then calculates the trimmed mean of the submissions by removing the highest and lowest figures and averaging the remaining values.

In 2012 allegations of rate fixing were published by several media outlets, including the Financial Times and the Wall Street Journal. The panel banks were accused of purposely submitting artificially low or high-interest rates to force LIBOR either higher or lower. Because a substantial portion of derivatives was priced using LIBOR, a move in either direction allowed banks to earn significant profits depending on their derivative position. By manipulating LIBOR rates, these banks were not only impacting the prices of derivatives but also mispricing other financial assets like home mortgages and student loans. Public outrage over this revelation led regulators to fine banks that were involved in the scandal more than 9 billion dollars and highlighted the flaws many did not realize were present in LIBOR. Regulatory bodies began devising plans to shift away from LIBOR to more appropriate rates to prevent this from occurring again.3

What are the other options to replace LIBOR?

In the wake of the LIBOR scandals, the Federal Reserve Board and the New York Fed decided to convene the Alternative Reference Rates Committee (ARRC). The objective of the ARRC was to identify a suitable replacement for LIBOR and assist with the transition away from the rate. In 2017 ARCC named the Secured Overnight Financing Rate (SOFR) as the rate most suitable for replacing LIBOR in the use of derivatives and other financial contracts. Unlike LIBOR, which is calculated based on a survey of panel bank estimates, SOFR is calculated from actual market transactions in the Treasury Repo market, one of the world’s deepest and most liquid markets.4 This prevents SOFR from being manipulated in the same manner as LIBOR.

Outside of SOFR, other reference rates have also emerged as potential replacements for LIBOR. Another alternative is the Bloomberg Short-Term Bank Yield Index (BSBY). BSBY was developed by Bloomberg L.P. in 2021 and is a series of interest rate benchmarks based on unsecured lending in short-term credit markets. The yields that determine the BSBY are derived from Commercial Paper, Certificate of Deposits, USD Bank Deposits, and Corporate Bonds. Unlike SOFR, which is based on collateralized treasury repurchase agreements, the BSBY relies solely on a range of unsecured loans that more accurately capture the borrowing costs of small to medium regional banks.5 Bloomberg has asserted that BSBY can supplement SOFR in the transition from LIBOR by helping banks better understand their financing costs.

As the transition from LIBOR reaches its conclusions and more reference rates become available, the ARRC encourages all market participants to “know” their alternative reference rate. The ARRC puts out best practices that highlight what investors should consider when selecting a reference rate:

- Understand how the financial benchmark is constructed and what the associated risks are

- Assess and ensure the benchmarks stand up to the IOSCO Principles

- Evaluate whether the benchmark being used correctly aligns with its intended purpose6

As the loop on LIBOR comes to a close, these alternative reference rates should provide investors with viable options to choose from when it comes to securing loans or participating in the derivatives market.

As always, feel free to reach out if there are any questions on how to navigate these changes.

- Quarles, Randal K. “Goodbye to All That: The End of LIBOR.” Board of Governors of the Federal Reserve System, 5 Oct. 2021, federalreserve.gov/newsevents/speech/quarles20211005a.htm.

- Hou, David, and David Skeie. “Libor: Origins, Economics, Crisis, Scandal, and Reform.” Federal Reserve Bank of New York, Mar. 2014, newyorkfed.org/medialibrary/media/research/staff_reports/sr667.pdf.

- Fernando, Jason. “What Was the LIBOR Scandal? What Happened and Impacted Companies.” Investopedia, Investopedia, 12 June 2022, investopedia.com/terms/l/libor-scandal.asp.

- “Progress Report: The Transition from U.S. Dollar LIBOR.” Federal Reserve Bank of New York, 31 Mar. 2021, newyorkfed.org/medialibrary/Microsites/arrc/files/2021/USD-LIBOR-transition-progress-report-mar-21.pdf?442.

- Hayes, Adam. “Bloomberg Short-Term Bank Yield Index (BSBY).” Investopedia, Investopedia, 25 Jan. 2023, investopedia.com/bloomberg-short-term-credit-sensitive-index-6281551.

- “Alternative Reference Rates Committee Guide to Published SOFR Averages.” Federal Reserve Bank of New York, 11 May 2021, www.newyorkfed.org/medialibrary/Microsites/arrc/files/2021/20210511-guide-to-published-sofr-averages