Mid October Update

October, historically a sometimes volatile month for the stock market (the crash of 1929 and 1987 helped form that reputation), has proven challenging in 2018 as well. Though far from a crash, we are experiencing a repricing of stocks and bonds on a global basis. On October 11th the Dow industrials dropped 831 points followed by a 546 point decline the next day.

The selling has been led by technology and strong momentum (think “over-loved”) names. These stocks tend to have large embedded growth expectations built into their stock prices as demonstrated by very high Price/ Earnings multiples. The problem is some of the support for these lofty valuations is attributable to a low and flat to declining interest rate environment—that environment no longer exists courtesy of the Federal Reserve (Fed) and its pre-determined agenda to “normalize” interest rates (more on that later).

Netflix Tonight?

For TV bingers “Netflix Tonight?” is not an unfamiliar email to pop up in your inbox, but it’s important to separate the investment thesis and valuation from our enjoyment or use of the product. In our last quarterly letter, we mentioned our valuation concerns regarding the “FANGMAN” stocks (plus Tesla-we will revisit Tesla later as well).

Let’s check on the recent declines from their respective 52-week highs to the respective market closing prices on Oct 12th:

- Facebook down 29%

- Amazon down 14%

- Netflix down 18%

- Google down 14%

- Microsoft down 7%

- Apple down 7%

- Nvidia down 16%

- Tesla topping them all down 32%.

- As a comparison, the Dow Industrials were down approximately 6%.

A New Sector

The ways in which we communicate and consume information have changed greatly, as have the ways we invest in these companies. For a more accurate representation of how today’s telecommunications, media and internet companies relate to one another and the broader economy, the Global Industry Classification Standards (GICS) has instituted changes to the S&P 500 sector classifications effective Sept 28th, 2018, the first major change since 1999.

The new Communication Services sector will include companies involved in social media, cable, broadcasting, telephone, gaming and advertising. In making this change, Standard & Poor’s/Dow Jones removed thirteen companies from the Consumer Discretionary sector and six from the Information Technology sector. Facebook and Alphabet make up 40% of the Communications sector. These two companies plus Disney, Netflix and Electronic Arts comprise 55% of the new sector – all doing their part to change the way we communicate and receive entertainment. Should, in our view, an appropriate margin of safety be priced in, where suitable, we would consider building out an appropriate position via this new sector fund.

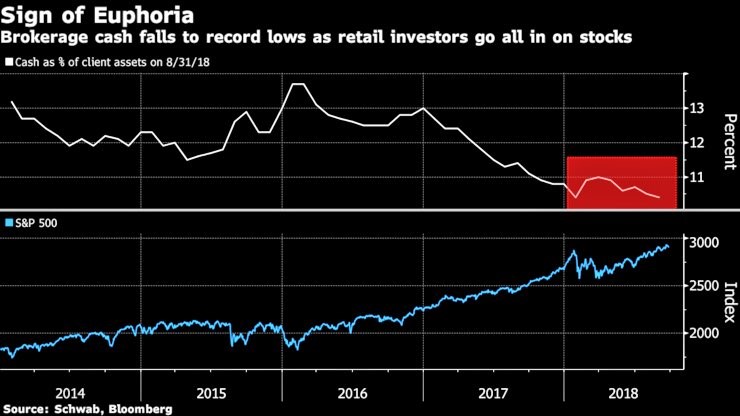

Mom & Pop Late to the Party?

US stocks had a strong third quarter, luring some retail investors back into the longest bull market on record. Retail investors poured cash into the market during a quarter in which all major US benchmarks reached record highs. Investor sentiment and expectations, from a contrarian perspective, is a concern and indicative of a market that may need to reset expectations and valuations. Some of the reset may be in motion as of the writing of this piece.

Source: Holger Zschaepitz

Anticipation of a post-midterm election bump may help ease some investor concerns. During mid-term election years going back to WWII, stocks have tended to rally in the final quarter of the year. Political drama in Washington, increasing oil prices, trade war escalation and a scare related to higher interest rates are all concerns that should not be ignored. However, if progress is made on any of these fronts, and/or Q3 reported earnings exceed expectations, it would not be surprising to see a positive bounce in the market.

High on Cannabis Stocks, Hung Over on Bitcoin?

The emergence of new stock market crazes is confirmation that gambling instincts for some investors can only be repressed for so long. The crypto craze, which we previously talked about, seems to have faded, at least for now. From a December 2017 peak of about $20,000, Bitcoin’s price has toppled 69% to $6,200, leaving many of the Bitcoin bulls searching for answers.

Are pot stocks the new Bitcoin?

Investor optimism about the prospects for cannabis and related products (both for medical and recreational uses) has most of these stocks in apparent bubble territory. Tilray, a Canadian maker of cannabis extracts, skyrocketed 94%, after its CEO indicated they had received an approval to import marijuana for a medical study. Fifty-three minutes and four trading halts later the stock was negative only to rally higher and end in the black. Anyone purchasing the stock late in the day could have lost over 90% of his/her investment. At its peak, Tilray was valued at $30 billion- that’s more than Twitter, CBS and American Airlines (where you can safely fly high). Interestingly, Tilray compares poorly with larger, more established leaders with the highest cost of goods sold per gram. Perhaps investors that purchased Bitcoin (and marijuana stocks) at the wrong time, can now use Tilray’s products to ease some of the pain. Unlike the new Communications sector we don’t anticipate seeing an attractive risk return outcome for pot stocks any time soon.

Speaking about smoke, what is Elon Musk smoking?

The Securities and Exchange Commission (SEC) filed fraud charges against Elon Musk, Tesla’s Chief Executive Officer, after a series of tweets having secured funding for taking the company private. The SEC suit, which was quickly settled, has Elon Musk stepping down as chairman of the board for three years and paying a $20M fine, but allows him to remain as the company’s CEO. This is yet another example about how the lack of proper corporate governance and board oversight can lead to unacceptable outcomes for a company and its shareholders.

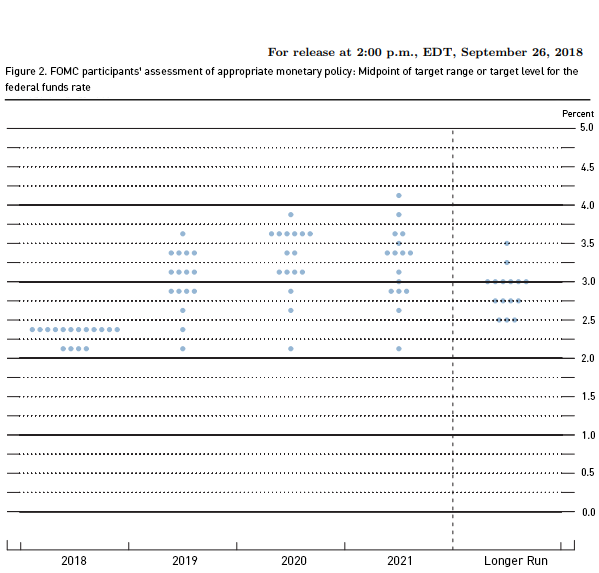

Neutral on Rates?

Recent Fed talk has indicated less agreement on what is a “neutral rate” as a guide for monetary policy. The neutral or “equilibrium” rate is the federal funds rate that neither stimulates nor restrains economic growth. Fed policymakers differ on where they see the neutral rate of interest with current estimates ranging from 2.0 to 3.5 percent.

After eight hikes since late 2015, the fed funds rate is now at the highest level since October 2008, just after the collapse of Lehman Brothers Holdings Inc. As the Fed continues to tighten, the market’s focus has increasingly turned to when the Fed will stop raising rates. The median forecast of FOMC officials in September called for interest rate increases to continue into 2020, rising from 3.1% at the end of 2019 to 3.4% at the end of 2020.

According to the Federal Reserve’s dot plot, a visual representation of where FOMC members expect rates to be in the short, intermediate and long term, there is still considerable uncertainty/ dispersion about the path of monetary policy. The September dot plot (see chart below) also reveals expectations for rates to shoot higher than the neutral rate – which means monetary policy would turn restrictive. It is important for the interest rate environment to continue to normalize, so the Federal Reserve can lower rates if needed to stimulate the economy. If the Fed makes a policy “error”, however by being too restrictive this could lead to what is referred to as a “hard landing” for the economy. Such an outcome would imply a recession and most likely a material correction for stock prices. Because of this potential for “overshooting”, the market will be closely monitoring Fed comments and actions.

Source: Federal Reserve

As 2018 reminds us yet again, greed, fear and market volatility will always be part of the investment equation. Market volatility can cause investors to decrease (and increase) stock exposure based on market moving headlines. In general, we encourage everyone to stay on plan. We will attempt to use market fear (and greed) in a way that allows us to best achieve your long-term goals. As always, we welcome your questions and comments. Should there be significant changes in your life or a desire to discuss any topic, please do not hesitate to reach out to us.