How does the Social Security Administration determine COLA?

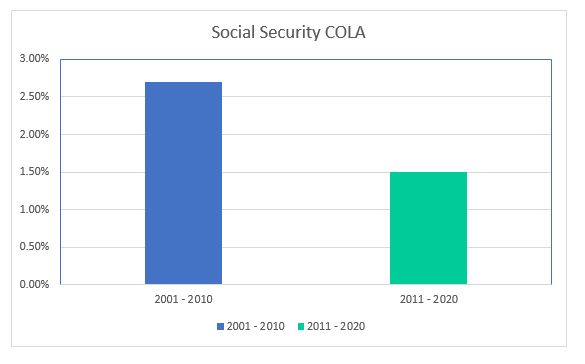

Inflation adjustments are based on increases in the CPI-W (Consumer Price Index for Urban Wage Earners and Clerical Workers) released by the Bureau of Labor Statistics. According to the Social Security website the average retired worker’s monthly benefit would increase from $1,523 to $1,543 beginning in January 2021, or only $20 per month more.

But do not ignore the bubbles, even if small. While a 1.3% increase in benefits may not seem like a significant amount it is important to recognize the power of an inflation-adjusted stream of income. For workers who wait to collect benefits until Full Retirement Age, which is based on year of birth and runs between 66 and 67 years old, the maximum monthly benefit is $3,011*. For a married couple where each spouse paid into the system over the course of their careers that equates to more than $72,250 annually – likely more than many would guess. The present value of those payments, assuming a life expectancy of approximately 18 years (mortality rates used by Social Security for someone currently aged 66) would be over $1M! Let’s remember that while corporate or state pension benefits are also a valuable component for families that receive them, they are rarely adjusted for inflation and lose purchasing power over time.

How can you Optimize Benefits and What about the future of Social Security?

For those who are skeptical about the future viability of the Social Security system we will be the first to acknowledge that Congress needs to make a series of adjustments to ensure the program lasts for decades to come. In fact, these potential adjustments would call for a separate article. However, when it comes to longevity risk, income is an important part of the equation, which presents us with an interesting dilemma: should we take benefits early or wait? Each year someone can delay electing benefits helps to increase those inflation-adjusted monthly payments. For someone whose full retirement age is 66 the Social Security Administration will increase benefits by 8% each year she waits. Waiting to receive benefits until age 70 would produce a 32% increase over four years. Using our prior example of a $3,011 maximum benefit at full retirement age, waiting until 70 would increase the monthly benefit to $4,096 (or $98,314/yr. for a married couple). Of course, this must be balanced with individual cash flow needs and life expectancy. Choosing the right claiming strategy can be complex and should be evaluated on a case by case basis.

With the Federal Reserve signaling they may allow inflation to run hot, above their 2% target, taxpayers must pay attention to future years’ COLAs as we emerge from the economic burdens caused by the coronavirus pandemic. Here’s hoping for a bubblier future.

For further questions about Social Security and how to think about optimizing benefits please do not hesitate to contact your wealth advisor.

*Source: SSA.gov